The firms that make clients the happiest face a challenge in getting millennials to stick with them. That's the key takeaway from J.D. Power's 2018 U.S. Full Service Investor Satisfaction Study. The survey also identified out what hard-to-please millennials are going to demand as they come to dominate the marketplace — lots of personal interaction, not just high-tech tools. Financial firms were ranked based on a December survey of 4,419 investors who work with financial advisers for at least some of their investments. Firms were measured on a 1,000-point scale based on how they fared in categories including account information, investment performance, firm interaction, product offerings, commissions and fees, information resources and problem resolution. No. 10: Northwestern MutualScore: 839 With a score that came in precisely at the average of all firms, Northwestern Mutual made it to the Top 10. If it's any consolation, the firm's score was higher than the 838 that won Schwab top honors last year. The Northwestern Mutual is an American financial services mutual organization based in Milwaukee. The financial security company provides consultation on wealth and asset income protection, education planning, retirement planning, investment advisory services, trust and private client services, estate planning and business planning. Its products include life insurance, disability income, and long-term care insurance; annuities; investments; and investment advisory products and services. Type Private (Mutual) Industry Financial Services Founded 1857 Headquarters Milwaukee, Wisconsin Key people John Schlifske, chairman and CEO, Greg Oberland, president Products Insurance and investments Revenue Increase$28.158 billion USD (2016)[1] Net income Increase $818 million USD (2016) Number of employees 7,500 (2017) Website www.northwesternmutual.com No. 9: Raymond JamesScore: 842 The firm slipped from eighth place in last year's survey, but its satisfaction score was much higher than the 819 it posted last year. Raymond James Financial is an American diversified holding company providing financial services to individuals, corporations and municipalities through its subsidiary companies that engage primarily in investment and financial planning, in addition to investment banking and asset management. Type Public Traded as NYSE: RJF S&P 500 Component Industry Investment services Founded 1962; 56 years ago Founder Robert James Headquarters St. Petersburg, Florida, United States Key people Tom James (Chairman Emeritus) Paul Reilly (Chairman and CEO) Products Financial services, securities and insurance brokerage, investment banking, asset management, banking and cash management, trust services. Revenue Increase 6.37 billion USD (2017) Net income Increase $636.3 million USD (2017) Website www.raymondjames.com Nos. 8, 7 and 6: UBS, LPL and FidelityScores: 851 The three-way tie belies some key differences from last year. UBS, for instance, fell from fifth place last year, but its score rose from 827. Fidelity fell from its No. 2 position last year, but its score also rose — from 835. And last year, LPL wasn't among the Top 10. No. 5: Merrill Lynch Score: 852 The giant moved up sharply from ninth place last year, and its satisfaction score jumped from 819. Merrill Lynch Wealth Management is a wealth management division of Bank of America. The firm is headquartered in New York City, and occupies the entire 34 stories of 250 Vesey Street, part of the Brookfield Place complex, in Manhattan. Merrill Lynch employs over 15,000 financial advisors and manages $2.2 trillion in client assets. The firm has its origins in Merrill Lynch & Co., Inc. which, prior to 2009, was publicly owned and traded on the New York Stock Exchange under the ticker symbol MER. Merrill Lynch & Co. agreed to be acquired by Bank of America on September 14, 2008, at the height of the 2008 Financial Crisis.[5] The acquisition was completed in January 2009[6] and Merrill Lynch & Co., Inc. was merged into Bank of America Corporation in October 2013, although certain Bank of America subsidiaries continue to carry the Merrill Lynch name, including the broker-dealer Merrill Lynch, Pierce, Fenner & Smith. No. 4: RBC Wealth ManagementScore: 863 RBC is another instance of a firm making the Top 10 list this year after having a less-than-stellar ranking in 2017. For more than a century, RBC Wealth Management has provided trusted advice and wealth management solutions to individuals, families and institutions. We are a global organization, bringing our diverse expertise and deep knowledge to the sophisticated financial needs of our clients around the world. We are committed to earning our client’s trust by building lasting relationships and confidence, putting your interests first in everything we do. Every interaction with us is defined through our core values and culture of doing what’s right for our clients and the communities we operate in. Forward-looking, innovative and committed helping our clients thrive and communities prosper – we are the partner you can depend on to help you achieve your financial goals. No. 3: Stifel Nicolau Score: 865 The firm improved its leadership position, moving up from last year's sixth spot and its 2017 score of 826. Stifel Financial Corp. (NYSE: SF) is a financial services holding company created under its present name in July 1983 and listed on the New York Stock Exchange on November 24, 1986. Its predecessor company was founded in 1890 as the Altheimer and Rawlings Investment Company and is headquartered in downtown St. Louis, Missouri. Stifel offers securities-related financial services in the United States and Europe through several wholly owned subsidiaries. Its clients are served through Stifel, Nicolaus & Company, Incorporated (Stifel Nicolaus) in the U.S., a full-service retail and institutional brokerage and investment banking firm, through Stifel Nicolaus Canada Inc. in Canada, and through Stifel Nicolaus Europe Limited (SNEL) in the United Kingdom and Europe. Its other subsidiaries include Thomas Weisel Partners LLC (TWP), Century Securities Associates, Inc. (CSA), an independent contractor broker-dealer firm, and Stifel Bank & Trust, a retail and commercial bank. The company's broker-dealer affiliates provide securities brokerage, trading, investment banking, investment advisory, and related financial services to individual investors, professional money managers, businesses, and municipalities. Stifel Bank & Trust offers a full range of consumer and commercial lending solutions. Stifel Trust Company, N.A. offers trust and related services. Type Public Traded as NYSE: SF S&P 400 Component Industry Investment services Founded 1890; 128 years ago Headquarters St. Louis, Missouri, U.S. Key people Ronald J. Kruszewski (Chairman of the Board, President, and CEO) Products

Revenue US$ 2.2 billion (2014) No. of employees 5,266 (2012) Website www.stifel.com No. 2: Edward JonesScore: 866 The St. Louis-based giant inched up from the No. 3 spot last year and improved its satisfaction score from 833. Edward D. Jones & Co., L.P., since 1995 simplified as Edward Jones is a financial services firm headquartered in Des Peres, Missouri, United States and serves investment clients in the U.S. and Canada, through its branch network of more than 14,000 locations and currently have relationships with nearly 7 million clients and $1 trillion asset under management worldwide. The firm focuses solely on individual investors and small-business owners. Edward Jones is a subsidiary of The Jones Financial Companies, L.L.L.P., a limited liability limited partnership owned only by its employees and retired employees and is not publicly traded. Type Partnership Industry Investment services Founded 1922 Founder Edward D. Jones Headquarters Des Peres, Missouri, United States Revenue US$6.632 billion (2016) Net income US$746 million (2016) Total assets US$19.424 billion (2016) Number of employees 43,000 (2016) Parent The Jones Financial Companies Website www.edwardjones.com No. 1: Charles SchwabScore: 867 Schwab not only retained the lead position that it held last year, it also increased its customer satisfaction from a score of 838. The Charles Schwab Corporation is a bank and brokerage firm, based in San Francisco, California. It was founded in 1971 by Charles R. Schwab and is one of the largest banks in the United States and is one of the largest brokerage firms in the United States. The company provides services for individuals and institutions that are investing online. The company offers an electronic trading platform for the purchase and sale of financial securities including common stocks, preferred stocks, futures contracts, exchange-traded funds, options, mutual funds, and fixed income investments. It also provides margin lending, and cash management services, as well as services through registered investment advisers. Type Public Traded as

Industry Financial services Founded 1971; 47 years ago (as Charles Schwab & Co., Inc.) Founder Charles R. Schwab Headquarters San Francisco, California, U.S. Number of locations 345 branches Key people

Services Brokerage firm Revenue US$8.62 billion (2017) Operating income US$3.65 billion (2017) Net income US$2.35 billion (2017) AUM US$3.36 trillion (2017) Total assets US$243.27 billion (2017) Total equity US$18.53 billion (2017) Number of employees 17,600 (2017) Website Schwab.com

0 Comments

1. Starbucks Brand value (in millions): $32,421 Last year's rank: 1 Value last year: $25,615 Percentage change from last year: +27 percent Starbucks was given top marks thanks to a Brand Strength Index of 89.2 percent, up 3 percent from 2017. Starbucks U.S. same-store sales increased just 2 percent in the first quarter, but it's global potential and growth is robust. China boosted revenues 30 percent in Q1, thanks in large part to the $1.3 billion record-setting acquisition of the remaining 50 percent share of its East China business. Comps were up 6 percent in China and there's no reason to expect that growth to taper off. CEO Kevin Johnson said in the Q1 conference call that China's GDP is expected by many economists to exceed $15 trillion by 2021. In addition to this, Starbucks is preparing to open 1,000 or so global retail Reserve stores and reignite its U.S. business through several tech-driven initiatives, as well as gain share of at-home coffee. What the Future Really Holds for Starbucks

Starbucks' new premium retail store in Seattle is part of the long-term growth plan. Much has been said about Starbucks’ slowing U.S. business in recent months. The company’s same-store sales increased 2 percent in the first quarter, which underwhelmed investors and even led one analyst to downgrade the coffee chain’s stock, as well as trim its price target to $64 from $67. For the first time since that 1Q report, Starbucks executives shared the brand’s strategy to revitalize these comps and offer perspective into what the company has accomplished during a transformational five-year period. Scott Maw, Starbucks’ chief financial officer, delivered a presentation to more than 200 analysts and investors as part of the UBS Global Consumer and Retail Conference. Maw highlighted the company’s six operational priorities for long-term growth, and also spoke about Starbucks’ efforts to stabilize and ignite U.S. sales. Needless to say, some major changes are coming. Here were some of the highlights. To start, Starbucks’ sheer size and infiltration into the marketplace has clouded its growth a bit. Customers understand it’s an accessible part of their lives, in nearly every market across America. And perhaps that’s muddied the story. A snapshot: in the past five years, Starbucks’ store count has increased from 18,066 to 27,339. It has gone from serving 61 million customers per week to 91 million. Revenue is up to $22 billion from $13 billion and the company’s market cap has ballooned from $39 billion to $78 billion. In explaining this growth story, Maw said Starbucks adjusted its operational procedures to not just meeting the rising customer base, but also to evolve with the industry on multiple fronts. He shared Starbucks’ six operational priorities:

Let’s focus on No. 1. About a year ago, Starbucks recorded a significant slowdown in traffic at peak. “It actually turned negative in our busiest stores that had a lot of MOP [mobile order and pay] transactions. And so, what we did is we focused on training on specific roles, on really getting the partners that were in the stores pointed at where the biggest activity was and where the biggest bottlenecks were,” Maw said. This bottleneck issue has been a critical one for Starbucks. Maw said the brand has used LEAN principles (this typically means creating more value for customers with fewer resources), and, within three months, began to see comps turn. “And they went from negative to flat to positive over a relatively short period of time. And actually for the last three quarters, those busiest stores that had the biggest challenges a year ago have actually grown comps faster than the average, and again that's that focus around operational excellence,” Maw said. Maw added that Starbucks saw its peak hold strong in the past quarter, despite the lower-than-expected comps. More so, for the first time in five years, Starbucks launched an update nationally to what it calls labor deployment known as Deployment 2.0. “But it's really how we position our partners at different dayparts within the store to drive throughput and service our customers,” he said. The old system, launched five years ago, was based on average product mix, food, beverage, and an average daypart mix. “But our stores aren't average. So, you can have stores that have 30 percent, 40 percent food, you can have stores that have 60 percent, 70 percent cold beverage, and you can have anything along that spectrum,” he said. Back then, Starbucks’ food was 15–16 percent of total sales. Now, it’s over 20 percent, Maw said. In some units it’s even gone from 15 to 30 percent over that five-year period. Cold beverages as a percent of total beverages was in the mid-30s five years ago. It’s above 50 percent currently. And again, Maw said, some Starbucks have seen the mix double. “And yet we were running the same plays and the same deployment based upon average from five years ago,” he said. So the new deployment, the 2.0 iteration, is organized daypart-by-daypart, store-by-store, mix-by-mix, Maw explained. The goal: having employees in the right places at the right time. Starbucks' beverage innovation will focus on core offerings, not short-term "sparks." "We haven't always grown as fast as perhaps we'd like to on the digital side. But that doesn't take away from the size of the opportunity." — Scott Maw, Starbucks chief financial officer. “We'll take a partner off a support role that they may be cleaning and restocking and we'll put them at the warming oven at peak because we know that store has a high mix of breakfast sandwiches at peak. Or where we might have had one partner on the espresso machine, then turning around and making cold beverages, we now have two partners working back to back servicing a high cold mix store,” he said. The new system is only three weeks in, but Maw said there has been positive employee feedback. “We've seen a tremendous amount of enthusiasm because it just makes sense. It frees them up to do what they should be doing and it makes them a lot more efficient. So, again, we used LEAN principles, we used training, we used a lot of the things we used—learned at peak to sort of optimize that and it's off to a good start,” he said. The tech side of Starbucks’ business remains a moving—and lucrative—target. Starbucks added 1.4 million Rewards members in the U.S. in Q1, up 11 percent year-over-year, bringing the total to 14.2 million active members. It’s about 15 million now, Maw said. Mobile payment in the U.S. has grown to more than 30 percent of total tender. This still leaves about 60 million customers, per month, who don’t have a digital relationship with Starbucks. “This isn't about Starbucks Rewards growth slowing. It's about an opportunity that is at zero today from a revenue standpoint on customers outside of rewards getting digital relationship,” Maw said. Starbucks has a three-pronged plan to capitalize on this opportunity—two that the company shared as being active and one it’s still investigating behind the corporate curtain. The first is opening up Mobile Order and Pay to all customers. Anyone who downloads the app will be able to order to ahead. Maw said this is coming by year’s end. “Everyone will have access to it. But today, a select customer base that downloads can order ahead. And when they do that, we obviously have the ability to capture their contact information and give them either in-app or e-mail marketing and start to track their spend behavior, so that we can then get them into the personalization engine and serve up offers,” Maw said. No. 2 is reactivating. That 15 million-customer pool is 90-day active, and there are millions of customers who are 91-plus-day active. “Those customers. We've been marketing to them for a while now and having some success in converting them, but we're going to go far deeper. The offers will be richer, because we know they pay off, and we're going to try to get that previously active base reactivated,” he said. Maw highlighted the third, which again, is in the experiment phase. This is what Starbucks calls WiFi signup. It looks like this: Guests who want to use Starbucks’ WiFi in stores enter an email once, and then every time they walk into the store it automatically connects to WiFi and you don’t have to accept the terms and conditions again. “It allows us to have the ability to have those e-mail addresses. And so, across those ideas and others that we're considering, we've said we'll have several million non-Starbucks Rewards digital relationships by the end of this year. And if you think about that 60 million, I would expect that number to continue to grow at a relatively rapid clip over the next handful of years,” Maw said. Maw said Starbucks is increasingly opening drive-thru locations “because that gets at an opportunity and an occasion for customers to have the faster experience, and our investment in throughput at peak, which has had a big pay-off for us over the last nine months or so, all goes to that kind of convenient side and the digital side of that spectrum.” It’s part of Starbucks’ plan to solve America’s retail puzzle. Another is the chain’s unique experiential nature. “If not more frequent and not as big a piece of the total timeframe, it becomes more important, that sense of connection, that sense of a place to engage with others and engage with our partners,” Maw said. Starbucks’ answer: Siren Retail. The term is an easier way to explain the Reserve Roastery and Princi development. Starbucks debuted its first Reserve store February 27 in Seattle, and plans to open 1,000 of these. Designed in an open, marketplace style, customers can engage with and order from employees at the Princi counter or Reserve coffee bar, then gather with family and friends at community tables or lounge areas around two fireplaces. Siren Retail also encompasses Starbucks Reserve bar locations, like the Shanghai and Seattle stores, and Princi bakeries. “What we believe is, if you look at—look in the retail world out there and certainly if you look in the restaurant retail world, there's not another brand out there with this many stores at scale that can win on both sides of this spectrum,” he said. “… We haven't fully executed on everything that we can. We haven't always grown as fast as perhaps we'd like to on the digital side. But that doesn't take away from the size of the opportunity, and I think that's important not to get lost in the monthly and quarterly view of U.S. comp.” On the innovation side, Maw said Starbucks’ “Sparks,” or short-term promotions (think crazy Frappuccino flavors) “just haven’t worked well” lately. “They haven’t paid off,” he added. “They haven’t paid back. Frappuccino Happy Hour is probably the biggest extreme of that, not really paying back. So, we're going to do very different things around Happy Hour this year. Basically, the Frappuccino Happy Hour that you know is going away and something new is coming in.” Starbucks is going to invest marketing dollars and time around core platforms. Nitro Cold Brew is an example. This was an extension of Starbucks’ popular cold brew platform. The company is currently testing items like Nitro tea lattés and Nitro milk lattes in some stores, which Maw said might or might not make it nationwide. Earlier in the year, Starbucks said it’s accelerating the rollout of Nitro cold brew from 1,300 stores currently to 2,300 restaurants in the U.S. by the end of 2018. CEO Kevin Johnson said the brand has seen about 1 point of additional comp growth in stores offering Nitro cold brew this past year. “But it's an extension of that core capability that we have, an extension of what customers already sort of know and love, and importantly in our stores, it allows us to market behind those platforms for longer,” he said. In January, the company launched its first new espresso in over 40 years with the Blonde offering. Maw said Starbucks has emphasized the product far longer than most of its launches—a sign of things to come with these core changes and more platform-based marketing. “Look for more things in Cold Brew, look for more things around Teavana iced teas, and we think that's a way for us to be able to extend core innovation of those platforms,” he said. In regards to food, Maw said Starbucks’ protein-forward Bistro Boxes and Sous Vide Egg Bits were successful launches. Recently, the company introduced a chicken sausage biscuit sandwich. On the growth side, Starbucks is targeting 750 openings. Average-unit volume in company-owned stores is $1.5 million, Maw said. Maw wanted to clear up what this growth plan really looks like. “I think a lot of the folks say that—look at that number and say, well, their comps are slowing, they must be moving sales from one store to another. But the reality is our licensed stores—and this is so important, our licensed stores and our company stores are different. They are not the same. It's not like we go into a downtown area and we open five licensed stores and five company-owned stores and they kind all look the same. They're totally different,” he said. Starbucks is opening 350 company-owned stores. Those licensed locations includes grocery stores, airports, Target, hotels, and other units that typically don’t feature outward facing doors. “Now, there's some sales transfer from licensed stores. I don't pretend that isn't the case, but it is just so much different and so much lower. I worry that sometimes we're not getting that message across. So, those licensed stores do not look like our company-owned stores,” he said. Sales transfer is what happens when Starbucks opens a company-owned store and sales and transactions move from one store to the other. Maw compared a store in Fort Collins, Colorado, without a drive thru doing 700 transactions, and one 2–3 miles away with a drive thru. “That existing store, before we opened it, had 700 transactions. A year afterwards, it had 600 transactions. The new store captured about 1,000 transactions. Again, that's the convenience of drive-thru, and about $2.5 million of revenue. So, this is just one year after. You can see the total transactions in the trade area went from 700 to 1,600 and revenue more than doubled. That's a highly profitable trade for us and it's all dependent on our ability to target real estate, have a minimal amount of sales transfer … What happens with this new store is it's going to comp at 2 times to 3 times the rate of the rest of the Starbucks stores. So, you're going to have three or four years built-up of stores that drive outsized comps. If I was to take the weighted average impact of those comps, it's meaningful compared to an average store. On the flip side, you obviously have negative comps in that existing stores, right. And if I take the weighted amount of that, it's a meaningful number. When I add those two numbers together, the lift from the new store and the comp impact from existing, it nets to basically zero.” This leaves virtually no impact on comps, Maw explained, since there’s an outsized comp in the new store offsetting the negative comps in existing stores. “It's all new on a relatively low ROI store, high profit beverage store, high AUV. It just works. We're not falling asleep on this. We're not closing our eyes and saying everything is good. We still look at it store by store. We learn from every store we open and we make adjustments,” he said. 2. McDonald's Brand value (in millions): $24,872 Last year's rank: 2 Value last year: $20,291 Percentage change from last year: +23 percent McDonald's topped the strongest brands index list at 89.9 to buoy its overall mark. It's growth over last year's rankings shows how the fast-food company's adjustments this past year have paid off. Despite reports that its new $1 $2 $3 Value Menu was slow out the gate, McDonald's still enjoyed a watershed calendar year. When McDonald's reported its fourth quarter and fiscal 2017 earnings in late January, shares were trading around $177—up an eye-opening 44.5 percent over the past year. The company's global comparable sales climbed 5.3 percent, giving the chain its best sales performance in six years. Systemwide sales were up 7 percent and McDonald's reported positive guest counts in all segments. McDonald's also said after the fourth quarter that it plans to invest about 52.4 billion of capital in 2018, the majority of which will go to deploying the "Experience of the Future" design at U.S. locations, and open about 1,000 new locations. So do not expect this momentum to slide anytime soon. 3. Subway Brand value (in millions): $8,083 Last year's rank: 3 Value last year: $8,400 Percentage change from last year: -4 percent The study pointed to Subways reduced revenue forecasts related to store closures as a reason for its decline, although it held firm at the No. 3 spot. There are a lot of changes underway at the 44,000-unit-plus brand right now, which serves about 7.5 million customers per day. Subway's domestic store count dropped by some 900 stores in 2017. That is still less than 4 percent of its nearly 26,000-unit U.S. presence. CEO Suzanne Greco said she expects closures to continue somewhat over the next three years as Subway shutters poor-performing stores and relocates others to more desirable locations. This as traffic patterns continue to shift. At the same time, Subway is rolling out its Fresh Forward design complete with vivid color palette, updated beverage stations, new ordering kiosks, and digital menu boards. Subway might absorb growing pains during this process, but it's clear the chain is making significant moves to remedy its largest concerns. 4. KFC Brand value (in millions): $8,049 Last year's rank: 4 Value last year: $6,155 Percentage change from last year: +31 percent As you can see by that healthy improvement, KFC's comeback story is in full effect. KFC has been a global power in recent quarters. Global same-store sales lifted 3 percent at KFC in Q4. Internationally, the chain showed robust 5 percent growth in international emerging markets and 3 percent in developed markets. KFC opened 539 new international restaurants in the quarter and 1,247 in 84 countries for the year, including 1,042 in emerging markets. The YUM! Brands chicken giant did report disappointing 1 percent same-store declines in the US. in Q4 and 1 percent growth for the year, marking four straight years of positive same-store sales. But KFC has several initiatives set to invigorate its stateside business. Included: the massive GrubHub partnership expected to bring delivery to thousands of restaurants. KFC also plans to remodel another 600 stores in 2018, resulting in nearly 40 percent of the base being updated by year's end. KFC's Comeback Story Takes Flight

The iconic big Chicken in Marietta, Georgia, embodies the kind of loyalty and enthusiasm the greater KFC brand is trying to capture. The Big Chicken silently clucks its beak and rolls its eyes. At 56 feet tall—about five stories—it peers over not just the nearby interstate, but almost all of Marietta, Georgia. At the chicken’s base, a marching band plays as people gather on an impromptu red carpet and take pictures. The mayor, Steve “Thunder” Tumlin, is at hand, dressed in an all-white suit. Beside him is a similarly clad man, this one a bit shorter and donning horn-rimmed glasses, a pointed goatee, and black necktie. Nearby, a “Little Chicken” mascot makes the rounds, posing with visitors. If it sounds like a circus has come into town, that’s because it has—or rather, it has returned after a short hiatus. In May, KBP Foods reopened the fabled KFC franchise location after closing in January for more than $2 million worth of renovations. The revitalized “Big Chicken” store is just one example—albeit a sizable one—of KFC’s latest play at reincarnation. Over the past decade, the fried chicken titan has watched its star decline as long-time adversaries like Chick-fil-A and Popeyes were on the upswing. Within the Yum! Brands family, KFC has lagged far behind top achiever Taco Bell and even trailed Pizza Hut, which has been beset with its own woes. But over the last couple of years, KFC has taken a multipronged approach to turning things around, proving that this bird still has some pluck in it. “As we started this brand turnaround, we really went back and started with, What’s the DNA of KFC? And what’s our brand positioning? And how do we bring this great, iconic brand to life in the U.S.?” says Brian Cahoe, chief development officer at KFC. “That’s the lens that we’ve taken everything through in this journey.” In 1991, the brand had jettisoned its original name of Kentucky Fried Chicken in favor of the snappier acronym. But as consumers find themselves nostalgic for days bygone, many brands are following suit, leaning back toward classic and authentic. For KFC, the decision to return to its roots also made sound business sense. “When Kentucky Fried Chicken was at its best and growing the fastest, the colonel and his values were at the center of everything we did. … Those values are critical to what makes Kentucky Fried Chicken so great,” says Kevin Hochman, brand president and chief concept officer. Hochman, who was promoted from chief marketing officer earlier this year, helped spearhead the company’s comeback. It seems fitting that a marketing specialist would be such an integral player in KFC’s renewed growth; after all, Harland “Colonel” Sanders called himself the No. 1 chicken salesman. At first glance, KFC’s turnaround might appear as nothing more than smoke and mirrors: off-the-cuff ads, flashy new flavors, and refurbished stores with screaming-bright colors. But for all of its staging, the process has been a serious one with high stakes. Over the past six years, the company has closed more than 1,000 domestic stores. Ten years ago, KFC ranked No. 7 on the QSR 50, besting the likes of Chick-fil-A and sister concept Pizza Hut with system-wide sales of $5.3 billion. Today paints a very different picture. Like many other legacy brands, KFC did not fare so well through the Great Recession as emerging fast casuals presented a more indulgent yet economical option for cash-strapped consumers. But for the first time in nearly a decade, the vitals are showing signs of recovery. Over the past two fiscal years, system-wide sales have finally grown, and the brand has posted 11 consecutive quarters of same-store sales growth. KFC also climbed one spot on the QSR 50 list this year (owing in no small part to the lingering damage from Chipotle’s food-safety woes, which knocked it down a rung). Skeptics might dismiss these numbers as an anomalous bright spot in an otherwise dim future, but other brands have proved it’s possible to surmount the odds. “It’s tough to take a legacy brand and turn that big ship in the right direction. It’s not easy to do that, but [KFC] is doing it well,” says Tim Hackbardt, CEO of BrandTrip Partners, a consulting group that works with restaurant groups. “Similarly, Arby’s has been doing a fantastic job. I think those guys are right in that same space. … They’re legacy brands, and they have good stories in there. [KFC] is very similar; they’re just a little behind that Arby’s curve.” So what are the keys to KFC’s reinvention? While not an exhaustive list, its efforts can mostly be distilled into three categories: branding and marketing, menu development, and design, including the functional and the flamboyant. A crowd of Colonels Wallpaper. That’s how Hochman describes the KFC’s TV ads before today’s campaign of colonel-clad celebrities. The commercial featured an Orlando-based KFC cook hand-breading and frying the chicken on-site. “Nobody even noticed it,” Hochman says. “We have to meet the customer where they are. They want to be entertained or they want something that’s going to get their attention, because if you don’t get their attention, it doesn’t matter what you’re saying.” Accordingly, the company transitioned to an education-plus-humor strategy and tapped “SNL” alum Darrell Hammond as the first in what has since proved to be a long string of Colonel impersonators. Although some consumers were initially perplexed by the whole campaign, KFC’s brand engagement is stronger than it’s been in years. The company’s own internal testing suggested that only 43 percent of fast-food ads were correctly linked to the corresponding brand. Thanks to the new Colonel ads, KFC’s numbers were close to double that (74 percent), Hochman says. He expects the series of ads will be a “slow burn” over time, meaning the rotation of Colonels isn’t going to slow any time soon. In one of the more recent commercials, actor Rob Lowe puts a tongue-in-cheek spin on JFK’s famous space-race speech, asserting that KFC would put a sandwich into space. The company made good on its promise; in June, it launched a chicken sandwich into the Earth’s stratosphere with a high-altitude balloon from private space-aiming company World View Enterprises. If launching a sandwich into space seems a bit excessive, remember this is the same brand that built a logo large enough to be picked up by satellites in 2006. Like Sanders himself, KFC subscribes to a go-big-or-go-home philosophy. It’s a major asset, one that the brand has learned to yoke other company initiatives to. Hackbardt is full of praise for the commercials and says he could see the series continuing for years. “What they’ve created here is an episodic marketing campaign worth tuning into, worth finding, and ultimately—the big part—worth sharing,” he says. “How often do you get a marketing campaign where people are actually seeking it out and listening and wanting to know when the next one’s coming out? It’s a beautiful thing.” The overall dilution of media means it’s especially difficult for advertisers to reach their audiences, Hackbardt adds. Like many companies, KFC has made a big push into the world of social media to woo uninterested young consumers who make up a steadily growing slice of the consumer pie. Globally, the brand boasts more than 46 million followers on Facebook, while the U.S. Twitter feed is nearly 1.2 million. In the past two years, the TV ads have garnered more than 160 million views on Facebook and YouTube. “Our intent is to make the brand younger over time while still making sure we’re driving our core customer base,” Hochman says. “Obviously, young people don’t watch and consume as much TV as older customers do. We still have to reach them … and so, in order to do that, we had to diversify our marketing investments across several media, and not just TV.” Already the move is showing promise. Hochman says that three years ago, before the turnaround began, three out of five millennials had never tried KFC. According to data from YouGov, the brand has since posted a 45 percent increase in millennial consideration. Southern, spice, and everything nice KFC’s zany new marketing strategy may pander to a certain consumer group, but it is not a simple case of lip service. The company also got down to the, uh, meat of its business. Like all facets of the brand revamp, the menu tweaks play at the retro and the über-trendy in tandem. On the traditional side, Hochman says, it was important to focus on something that would excite franchisees and customers alike: the Original Recipe with its proprietary blend of 11 herbs and spices. Amid an industry in flux, the Original Recipe chicken remains the No. 1 item to bring guests into KFC, followed by its box meals, Hochman adds. At the same time, the menu required more than its star attraction to stay relevant. “Younger people and their eating habits don’t necessarily lend themselves to eating chicken on the bone. Many meals are consumed in a car or on the go, which [makes it] harder to eat,” he says. “Our Original Recipe will always be our bestseller … but we are going to need to diversify beyond that.” To the brand’s credit, it has made several attempts to do just that—it just hasn’t been able to stick many landings. In 2009, the Fiery Grilled Chicken piqued interest; a year later, the Double Down—a sandwich with fried chicken fillets standing in for bread—turned heads (and some stomachs). In response to industry-ubiquitous chicken tenders, KFC fried up Original Recipe Bites. It’s even tried to challenge Chick-fil-A’s no-bones-about-it dominance with the Original Recipe Boneless Chicken. None succeeded, and none have a spot on the menu today. Despite a near decade of misses, KFC might have finally hit the mark. In early 2016, it became the first major fast-food brand to incorporate the regional favorite Nashville Hot into its menu. KFC even sent a food truck out on a two-week journey around the country to build buzz around the limited-time offer. The road trip also presented an opportunity for KFC to improve its foodie reputation. “The customer knows a higher quality of food comes out of food trucks. They’re typically hand-prepared by chefs that are just starting out or can’t afford to have a restaurant,” Hochman says. “The reason we did the food truck for Nashville Hot was to communicate that.” To further tick up the quality quotient, KFC invested 100,000 hours retraining cooks to bring their techniques back to “Colonel standards.” In April, it also set a deadline to stop using chicken treated with antibiotics for human medicine by the end of 2018. The pledge is a couple of years behind competitors, but as KFC points out, it is the first major chain to make such a commitment for bone-in chicken. KFC hit gold again this year with another LTO. While steeped in regional flavors like its predecessor, the Georgia Gold Honey Mustard BBQ Chicken eschewed a strict template. “We did the Georgia Gold with the regional flavors of the Carolina mustards and the Georgia mustards, and created our own little homage to that,” says corporate chef Bob Das, who has been with KFC for about 17 years. Indeed, the new menu strategy is all about paying homage to Southern flavors and approaching them as Sanders would have himself. The brand’s not disregarding increasingly adventurous consumer preferences, though. “We’re trying to meet the demands of the customer. Obviously there are flavor seekers, and spice is a big thing. As you saw with Nashville Hot, we had people really craving that heat and that distinct flavor you can’t find anywhere else,” Das says. “Instead of trying these outlandish flavors typical to the Southwest or things that are even Pacific Rim or Latin flavors, we’re going to be right where we’re supposed to be [with] Southern-inspired.” To that end, the brand recently imported an international favorite, the Zinger Spicy Chicken Sandwich. First launched in Trinidad and Tobago in the mid-1980s, the Zinger has since expanded to 120 countries. Now KFC is testing its appeal stateside and farther afield (the Zinger is the sandwich the brand sent to the stratosphere). Again honoring Sanders and his palate, the Zinger adds hot spices to the proprietary 11-herbs-and-spices mix. For all its global fanfare and out-of-this-world aspirations, the Zinger is not a guaranteed slam-dunk. “[KFC has] always struggled with sandwiches for some reason,” BrandTrip Partners’ Hackbardt says. Whereas fast-casual players like Slim Chickens and Starbird extol the merits of their chicken sandwiches—cooked-to-order, buttermilk-marinated, purposely sourced, etc.—the Zinger isn’t sufficiently promoted, he adds. In the commercial featuring Rob Lowe, “hand-breaded” is only mentioned a single time. “If you take a look at the Zinger and the Double Crunch, there’s not a big story about that other than being hand-breaded.” Nevertheless, Hackbardt says it’s something that can be easily remedied; after all, the 77-year-old brand has great stories to tell. But for all the heritage, creativity, and adaptation to consumer trends, KFC holds one distinct advantage over the competitors: its buckets. “Bone-in chicken is something that’s great for a large party purchase. … They have that advantage, because there aren’t a lot of chains that are offering that,” Hackbardt says. “That drives the average check exceptionally high, because now we’re talking $20–$30 or even higher purchases. There are very few [quick serves] or fast casuals that are getting those kinds of purchases.” Putting on a show Marietta’s Big Chicken may be an outlier, but it is representative of big changes throughout the system. Last year, KFC announced its “Re-Colonelization” plans, which encompass not only a recommitment to quality, but also a pledge to upgrade its stores. On the consumer-facing side, the brand combined the ostentatious with the inviting. Dubbed the American Showman style, the new design ratchets up the brightness of the exterior with bright red-and-white stripes, which were specifically designed to resemble a chicken bucket. The overall appearance is sleeker than older stores, and it manages to mix the old with the new: The iconic Colonel sketch remains, while block letters declaring KFC’s “World Famous Chicken” have been added. “If nothing happens to the exterior of your building, no one knows you did anything on the inside,” Hackbardt says. He recalls a focus group BrandTrip conducted for one of its limited-service clients; not a single participant could describe the interior of the restaurant, because they so rarely went inside. “To spend more money on the interior of your location doesn’t tend to pay off, because so much of your business goes through the drive thru.” Nevertheless, Hackbardt says a comfortable environment is always more inviting, especially if the company wants to encourage more dine-in business. The interior of the American Showman design also sports the signature color combo, but in a more understated manner. The Original Celebrity Chef wall sets old photographs of Sanders against a red background, pendant lights are interspersed around the store, and wood finishes on the tile floor and furniture imbue a warmth not uncommon in the fast-casual scene, but far rarer in fast food. The new stores even added a chalkboard to show the name of the cook working that day, as well as the farm from which the chicken was sourced. “There’s that flash of the Colonel boldness, carnival red-and-white atmosphere that draws your attention and creates that appeal to come in or go to the drive thru. But then we balanced that out with his pragmatic sensibilities, and certainly a real desire to have quality control on his products,” Cahoe says. Unlike the other turnaround efforts, the redesign falls squarely on the shoulders of franchisees. Company-owned stores account for just 4.8 percent of the domestic system, meaning it’s up to the operators to revamp their stores and make the American Showman style the default look of KFC stores. So far about 500 locations (a little over 10 percent) have made the upgrade. Cahoe says the plan is to have the new design in 70 percent of stores around 2020 since franchisee obligations come up for renewal within different time frames. “The partnership and the change with the franchise system arguably happened on the front end of all this. I don’t know that we would have the traction in the turnaround … if we didn’t have that relationship and partnership in place upfront,” Cahoe says. “You’ll hear a consistent theme that the relationship has never been stronger—and you need the strength of that relationship to have the type of success that we’re having in the space.” Thankfully, franchisees like KBP Foods are jumping in head first. The company plans to upgrade dozens of units and employ the new design with all future growth. As for the Big Chicken location, it required a higher price than building a completely new store. But considering what a beloved fixture it is in the community—and the larger KFC system—the price seems well worth it. From the adjoining gift shop to the statue of Colonel Sanders to its very own AM radio station featuring “deep thoughts from the previously silent bird,” the Big Chicken has the pop-culture prowess and deep connection to consumers that KFC is still chasing. But if the legacy brand can maintain this newfound momentum, the famed Marietta location will be just one of many feathers in its cap. “We’re still on this journey. We know that we have a long way to go to get to where we all want to be, our north star,” Hochman says. “Despite having very good success the last few years, Kentucky Fried Chicken’s best days are still ahead of us.” 5. Tim Hortons Brand value (in millions): $5,033 Last year's rank: 5 Value last year: $4,108 Percentage change from last year: +23 percent Restaurant Brands International's chain came in as the fifth best brand in Brand Score Index at 83. Tim Hortons has no shortage of brand equity in Canada. U.S. growth has turned out to be a challenge for the Burger King and popeyes parent, however. Tim Hortons posted comparable same-store sales growth of 0.1 percent in Q4 and 0.1 percent declines in fiscal 2017. The chain has sped up its international growth. Tim Hortons opened its first restaurants in Asia, Europe, and Latin America, in fiscal 2017. The chain achieved 3 percent systemwide sales growth for the year, primarily driven by net restaurant growth. In the U.K., and the Philippines, RBI opened 13 and 10 restaurants in 2017 respectively, and also opened its first two restaurants in Egypt, Spain, and Mexico. "These international stores continue to perform well and our partners have been building robust pipelines for additional openings in 2018 and beyond. We continue to work closely with these partners to accelerate development in these international markets over time," chief technology and development officer Josh Kobza said in a conference call. 6. Domino's Brand value (in millions): $4,846 Last year's rank: 6 Value last year: $3,983 Percentage change from last year: +22 percent Another strong year widened Domino's gap as the most valuable pizza chain in the world. The brand posted same-store sales growth of 3.8 percent and 4.2 percent at company-owned and franchised stores, respectively, in Q4. These numbers actually underwhelmed Wall Street, which shows you the kind of calendar year Domino's had. For fiscal 2017, Domino's domestic comps increased 7.7 percent, making it 27 consecutive quarters of positive domestic same-store sales growth. Despite the fact Q4 was the chain's lowest quarterly growth rate in four years, Domino's has built momentum on top of momentum in recent reports, especially overseas. Comps growth of 2.6 percent gave Domino's 96 consecutive quarters of positive international sales gains. The company attributed its numbers to both a more volatile international market and sales dilution across an expanding system. Domino's only closed 13 stores domestically and 62 abroad, collectively the lowest level in two decades. The fourth quarter ended with a net addition of 422 stores. One note of uncertainty: the company will forge ahead without president and CEO J. Patrick Doyle, who was instrumental in the brand's turnaround since taking over in 2010, When he assumed the role from David. A Brandon, who stepped down March 7, 2010, Domino's shares were trading for $11.90 on the stock market. They were sitting at $227.47 midday Monday. Domino's board of directors announced that Richard Allison, 50, the president of Domino's International, would succeed Doyle as CEO. 7. Burger King Brand value (in millions): $3,150 Last year's rank: 9 Value last year: $2,568 Percentage change from last year: +23 percent RBI's Burger King brand is another fast-food icon enjoying a strong surge of late. The chain reported impressive comparable same-store sales growth of 4.6 percent in the fourth quarter. Perhaps even more notable: Burger King's comparable sales stateside were up 5.1 percent in the fourth quarter compared to just 1.8 percent in 2016. Right now, Burger King is thriving in the value wars thanks to a balanced approach. Schwartz said the brand's Bacon King and Crispy Chicken Sandwich lit up sales in 2017. Success could be seen across the board. Systemwide sales growth was 12.3 percent in the three months ended December 31. Burger King posted 6.5 percent net restaurant growth compared to 4.9 percent in the year-ago period. There were 7,226 Burger King in the U.S. as of December 31 after the company added a net of 70 new restaurants. Internationally, Burger King was strong as well. The chain ended 2017 with more than 875 restaurants in China, up from about 650 at the end of 2016. Burger King opened its 500th restaurant in Russia this past year and closed 2017 with more than 520 units—growth of about 100 restaurants. France grew its footprint over 200 locations. Brazil ended 2017 with nearly 700 locations compared to about 600 the prior year. 8. Pizza Hut Brand value (in millions): $3, 101 Last year's rank: 7 Value last year: $3,295 Percentage change from last year: -6 percent Pizza Hut took its lumps early in the year as it began to transform. But results began to shine through in the later part of the fiscal calendar. In Q4, global same-store sales lifted 1 percent and were flat for the year. Its U.S. comps hiked 2 percent in the fourth quarter. Pizza Hut had posted five consecutive quarters of declining sales before turning positive in the third quarter. Back-to-back growth quarters is a direct reflection of YUM!'s $130 million plan to reinvigorate Pizza Hut announced last spring after the company’s same-store sales dropped 7 percent in the U.S. in Q1. Some improvements: the chain rolled out 145,000 new pouches made with 3M Thinsulate Insulation thermal technology designed to deliver pizza 15 degrees hotter. Pizza Hut also hired 14,000 delivery drivers in 2017 and there are now more than 24,000 new car toppers on the road. The Hut Rewards program was launched in August. Growth wise, Pizza Hut opened 340 new international restaurants in Q4 and 826 units in 77 countries, including 592 restaurants in emerging markets. It wouldn't be surprising to see Pizza Hut climb back up the charts next year. 9. Dunkin' Donuts Brand value (in millions): $2,677 Last year's rank: 10 Value last year: $2,401 Percentage change from last year: 1 percent Dunkin' has a pretty bold three-year plan: 18,000 total IJ.S. units, including about 1,000 new stores in the next two—more than 90 percent of which will be built outside of its Northeast base. When you consider how much Dunkin' is growing right now, and how it plans to enter markets where it doesn't have a strong presence, you can understand some of the other changes. Like Dunkin's decision to drop the "Donuts" off the branding in certain new locations. Dunkin' sees this opportunity as a chance to win in categories it's historically not given credit for—places beyond convenience and breakfast. Dunkin' wants to chase afternoon guests with Dunkin' Deals (a medium hot or iced latte for $2 from 2 to 6 p.m. is one such offer). It also expects to play a larger role in the craft coffee culture With Cold Brew, additional espresso products, and an extension of its premium tea and frozen beverage lines. Also expect more sandwiches. On the previous note, however, Dunkin' isn't abandoning its breakfast and convenience strengths. In fact, the company is opening new next-gen stores with double drive thrus, where the second lane is for mobile orders. Its breakfast business has never been better, either. Currently, Dunkin's morning business accounts for about 60 percent of systemwide sales. That segment has reported positive for Dunkin year-over-year and increased sequentially each quarter in 2017. In the fourth quarter, Dunkin' posted same-store sales growth of 0.8 percent. 10. Chipotle Brand value (in millions): $2,541 Last year's rank: 8 Value last year: $2,935 Percentage change from last year: -13 percent Chipotle's post food-safety issues have been well documented. The burrito chain's comeback fluctuated but mostly dipped in the wrong direction last year. This after a promising first quarter that saw same-store sales boom 17.8 percent, year-over-year, and revenue jump 28.1 percent to $1.07 billion. This prompted Steve Ells to say Chipotle had made "incredible progress." But then the same tricks reared up. A Sterling, Virginia, location suffered a norovirus incident that affected more than 130 customers. A video of rodents falling from a ceiling went viral. An LA store was investigated for food safety. Even a TV actor took aim at the brand on Instagram. Legitimate or not, these public relations hits showed the sensitivity in Chipotle's armor. In early March, Chipotle's new CEO Brian Niccol, took the helm, with Ells moving to a chairman position. The former head of Taco Bell seems like a perfect fit given his resume as a marketing maven. Can he right the ship? Are new campaigns or value menu items coming? We will see soon enough. Can New CEO Brian Niccol Wake Up Chipotle?

What will former Taco Bell CEO Brian Niccol accomplish at Chipotle? It shouldn't take long to find out. When Chipotle announced Taco Bell’s Brian Niccol as the next CEO of the fast-casual burrito chain, RJ Hottovy was surprised. Not by the choice, but that it hadn’t been obvious all along. “I was kind of surprised that his name hadn’t popped up earlier as a potential candidate for the position,” says Hottovy, restaurant analyst at Morningstar. “As you look at success stories in the [quick-service] space, Taco Bell is certainly at the top of the list. Frankly, it was kind of interesting his name hadn’t popped up.” As CEO of Taco Bell, Niccol’s tenure was defined by unique menu innovations and bold marketing strategies that helped reposition the Mexican fast-food chain. Hottovy believes that experience should help him breathe new energy into Chipotle, which is still struggling to overcome food safety issues and lagging sales. “I think the biggest problem Chipotle’s had is there has really been no positive news for really three years,” Hottovy says. “Brian is the kind of guy who can find a way to bring some positive energy into the company.” Hottovy sees potential for Chipotle’s stock price to shoot up and down over the next year as Niccol makes his mark. He’s skeptical that it will reach its all-time high of more than $700 per share in 2015, but he thinks Niccol can at least deliver a stable stock price for investors. For consumers, he says, the concept has simply grown tired. Even new product launches—like Chipotle’s roll out of queso—came well after other competitors had unveiled their own versions. Overall, the look of Chipotle stores and menus have gone largely unchanged for years. “It pains me because I grew up two blocks from the original one in Denver,” Hottovy says. “So, I’ve been following this since day one. I was probably one of the first couple thousand customers at Chipotle.” Niccol’s selection underscores that Chipotle founder Steve Ells understands the brand needs more changes than he can orchestrate, Hottovy says. Ells, who founded the chain in 1993, announced in November 2017 that he would step down as chief executive as the brand looked for a new leader with “proven turnaround expertise.” In a Chipotle news release announcing the new hire, Ells said Niccol would help bring Chipotle to the next level, while also staying true to the brand’s values. “Brian is a proven world-class executive, who will bring fresh energy and leadership to drive excellence across every aspect of our business,” Ells said in the February 13 news release. “His expertise in digital technologies, restaurant operations and branding make him a perfect fit for Chipotle as we seek to enhance our customer experience, drive sales growth and make our brand more relevant.” In the news release, Niccol acknowledged that he would join Chipotle at a “pivotal time in its history.” He laid out plans to attract customers, return the brand to growth and deliver value for shareholders. “At Chipotle's core is delicious food, which I will look to pair up with consistently great customer experiences,” the new CEO’s statement read. “I will also focus on dialing up Chipotle's cultural relevance through innovation in menu and digital communications.” "I think the changes will be significant. They won’t be deck chairs moving around the Titanic. They will be a helicopter taking off from the back deck." — Gary Stibel, founder and CEO of the New England Consulting Group. Experts believe a value menu of some sort will be part of Chipotle's future. Gary Stibel, founder and CEO of the New England Consulting Group, applauded the selection of Niccol with some advice: “I would buy stock.” “And if I wasn’t going to buy stock, I’d just say this is the right person at the right time,” Stibel says. “This is a win-win for Chipotle. And candidly, it’s a little overdue.” He likened Niccol’s previous experience at Procter & Gamble to “basic training in the Marine Corps.” Alumni of such consumer packaged goods companies deeply understand supply chains, consumers and marketing strategies, he says. But moving from products to food service is often a difficult transition. “Here you’ve got a guy who crossed the chasm successfully. He is about the best pick we can think of for that job,” Stibel says. “And it’s important to make the change.” Stibel expects to see positive headlines for Chipotle soon. He predicts Niccol will push out announcements about new products, pricing or delivery options by the third quarter of 2018. “I think you will start seeing the new Chipotle. And I think the changes will be significant,” he says. “They won’t be deck chairs moving around the Titanic. They will be a helicopter taking off from the back deck.” One of Niccol’s biggest challenges will be to bring back once-loyal customers, Stibel says. He expects him to employ a new value proposition to drive traffic, but not one that resembles a fast-food dollar menu. “I think it will be a value menu for people who enjoy the quality of Chipotle and will react to value promotions,” he says. “What he needs to do is bring people back who left and stayed away and create a reason for those people still coming to Chipotle to come more often, spend more money and bring their friends.” Jason Moser, a stock analyst at the Motley Fool, expects the new CEO to reshape Chipotle’s brand identity with a refreshed marketing strategy (On March 14, 2018 Chipotle’s Chief Marketing and Strategy Officer Mark Crumpacker announced he would step down). For years, Chipotle has relentlessly leaned on its “Food with Integrity” pledge, highlighting the sourcing and quality of ingredients. “It seemed like whenever Chipotle wanted to do something on the marketing side it was always based on the quality of ingredients and putting themselves on a pedestal,” Moser says. “I think it’s going to be a very delicate balance he’s going to have to strike to help Chipotle bring a new marketing game to the market. But I also wouldn’t expect Chipotle to roll out a Doritos Loco Taco. We’re not going to see something beyond those lines, but I do think he’s going to bring more of an identity to Chipotle beyond just that food with integrity message.” While he doesn’t expect a traditional [quick-service]-style value menu, he believes Niccol will try to make some play at value. And he’s all but certain that Chipotle will roll out some new menu items to build excitement. And he says a new breakfast menu is almost a must at this point for Chipotle. “I’m stunned they haven’t yet. The name of the game in restaurants is traffic,” Moser says. “If you’re not selling breakfast, you’re telling the world that there are five or six hours of the day we don’t want your business, we don’t want you in our store.” Moser doesn’t expect the brand to abandon its focus on quality ingredients any time soon. But he believes the selection of Niccol must have been a “wake-up call” of sorts for Ells, who has often held up the quality of food at Chipotle against that of the value-driven fast-food chains. “My first reaction was kind of like, oh, the irony. It was a bit surprising to see that they would be bringing someone in from a concept like Taco Bell given the sort of the language Steve Ells had used in prior years,” Moser says. “He wasn’t very complementary of concepts like Taco Bell. I think he considered Chipotle a cut above them because of the food quality. So, I have to believe that was probably extremely hard for Ells to do. But I also thought that maybe he finally came to grips with the fact that he maybe doesn’t have what it takes to bring this business to the next level.” Source: Restaurant Magazine

Highlights:

|

RANK FRANCHISE | INVESTMENT |

| # 1 McDonald's | $1M - $2.2M |

| # 2 7-Eleven Inc. | $38K - $1.1M |

| # 3 Dunkin' Donuts | $229K - $1.7M |

| # 4 The UPS Store | $178K - $403K |

| # 5 RE/MAX LLC | $38K - $225K |

| # 6 Sonic Drive-In Restaurants | $1.1M - $2.4M |

| # 7 Great Clips | $137K - $258K |

| # 8 Taco Bell | $525K - $2.6M |

| # 9 Hardee's | $1.4M - $1.9M |

| # 10 Sport Clips | $189K - $355K |

| # 11 Jimmy John's Gourmet Sandwiches | $330K - $558K |

| # 12 Servpro | $158K - $212K |

| # 13 Culver Franchising System Inc. | $1.8M - $4.3M |

| # 14 Supercuts | $144K - $297K |

| # 15 Carl's Jr. Restaurants | $1.4M - $2M |

| # 16 Papa John's Int'l. Inc. | $130K - $844K |

| # 17 Anytime Fitness | $89K - $678K |

| # 18 uBreakiFix | $60K - $221K |

| # 19 Ace Hardware Corp. | $273K - $1.6M |

| # 20 Kumon Math & Reading Centers | $70K - $141K |

| # 21 Planet Fitness | $857K - $4.2M |

| # 22 Keller Williams | $184K - $337K |

| # 23 Budget Blinds LLC | $105K - $226K |

| # 24 Jersey Mike's Subs | $193K - $660K |

| # 25 Marco's Pizza | $223K - $664K |

| # 26 CPR-Cell Phone Repair | $58K - $176K |

| # 27 Primrose School Franchising Co. | $717K - $5.8M |

| # 28 Mathnasium Learning Centers | $103K - $144K |

| # 29 Hampton by Hilton | $6.9M - $17.1M |

| # 30 Snap-on Tools | $170K - $350K |

| # 31 Wingstop Restaurants Inc. | $347K - $733K |

| # 32 Pet Supplies Plus | $555K - $1.3M |

| # 33 Hilton Hotels and Resorts | $29.1M - $112M |

| # 34 Valvoline Instant Oil Change | $162K - $2.3M |

| # 35 Smoothie King | $226K - $778K |

| # 36 Matco Tools | $91K - $270K |

| # 37 HomeVestors of America Inc. | $44K - $347K |

| # 38 Merry Maids | $87K - $124K |

| # 39 Firehouse Subs | $95K - $1.1M |

| # 40 Mac Tools | $103K - $256K |

| # 41 Baskin-Robbins | $94K - $402K |

| # 42 Mosquito Joe | $67K - $128K |

| # 43 Jack in the Box | $1.5M - $2.9M |

| # 44 Freddy's Frozen Custard & Steakburgers | $593K - $2M |

| # 45 Massage Envy | $435K - $1M |

| # 46 The Maids | $76K - $164K |

| # 47 Pizza Hut LLC | $302K - $2.2M |

| # 48 Orangetheory Fitness | $488K - $994K |

| # 49 Right at Home LLC | $78K - $138K |

| # 50 Nurse Next Door Home Care Services | $105K - $199K |

Please contact us for a complete list from #51 to #150

5 Things To Do Before You Search For A Franchise

Financing Option:

The TGG’s Patron Incentives: To Be Determined (case by case) such as Initial Investment, Initial Franchise Fee, Net-worth Requirement, Liquid Cash Requirement. More details from The Global Gallery

Confidential Consultation: Contact us

The TGG’s Patron Incentives: To Be Determined (case by case) such as Initial Investment, Initial Franchise Fee, Net-worth Requirement, Liquid Cash Requirement. More details from The Global Gallery

Confidential Consultation: Contact us

Your preparation is the key. In other words, the time to get all your ducks in a row is not only an essential step for your success but it is also a tremendous gain an insight which will help to reduce your risk.

1. Start Reading & Studying.

Reading books on these topics will help you get a better understanding of business, and what it’s going to take to succeed. You want you to read books about:

1. Start Reading & Studying.

Reading books on these topics will help you get a better understanding of business, and what it’s going to take to succeed. You want you to read books about:

- Starting a business

- Entrepreneurship

- Franchising

- Business plans

- And if you really want to get a leg up, read an accounting book.

“The more that you read, the more things you will know. The more that you learn, the more places you’ll go.” – Dr. Seuss

2. Financials

Before you take the time needed to search for a franchise to buy, it’s important to see where you stand, financially. The best way to do it is by putting together a financial statement.

Generally speaking, the most time-consuming part of doing a financial worth statement is gathering all the information you need.

You’ll need your mortgage loan and credit card statements, information on all of your investments, and more. In a nutshell, you’ll need to gather everything that lists all of your assets and all of your liabilities.

Before you take the time needed to search for a franchise to buy, it’s important to see where you stand, financially. The best way to do it is by putting together a financial statement.

Generally speaking, the most time-consuming part of doing a financial worth statement is gathering all the information you need.

You’ll need your mortgage loan and credit card statements, information on all of your investments, and more. In a nutshell, you’ll need to gather everything that lists all of your assets and all of your liabilities.

3. Learn About Small Business Loans

If you’re like most of the people who are considering franchise business ownership, you’ll need a small business loan for the lion’s share of your startup capital needs.

That’s why it’s crucial to learn all you can about the types of loans that are currently available. And the information you need is only one-click away.

If you’re like most of the people who are considering franchise business ownership, you’ll need a small business loan for the lion’s share of your startup capital needs.

That’s why it’s crucial to learn all you can about the types of loans that are currently available. And the information you need is only one-click away.

4. Share Your Plan In Franchising With Your Family's Member

Transitioning from employee to franchise owner is a big deal.

That’s why it’s essential to discuss what you’re thinking of doing with the people who will be affected the most; your family.

And when you have the discussion, don’t hold back. Tell them why you want to be your own boss. Tell them how you’re going to get the money. Tell them how careful you’re going to be-and that you promise to do great research.

In the long run, as long as you’re upfront with them, and communicate with them during the entire process, chances are they’ll support your decision.

Transitioning from employee to franchise owner is a big deal.

That’s why it’s essential to discuss what you’re thinking of doing with the people who will be affected the most; your family.

And when you have the discussion, don’t hold back. Tell them why you want to be your own boss. Tell them how you’re going to get the money. Tell them how careful you’re going to be-and that you promise to do great research.

In the long run, as long as you’re upfront with them, and communicate with them during the entire process, chances are they’ll support your decision.

5. Eliminate Distraction

The last thing to do, before you start your search for a franchise opportunity is to eliminate all unnecessary distraction.

Specifically, take an internet-social media break. Spend a few months with you.

Refrain from answering emails, logging into your social media networks, or reading articles about franchising-or business. Instead, spend some time away from your Smartphone. Maybe you can spend time outdoors, or at least somewhere that will provide a change of scenery. But, it has to be distraction-free.

Doing what I just recommended will force you to take a hard look at what you’re thinking of doing.

The last thing to do, before you start your search for a franchise opportunity is to eliminate all unnecessary distraction.

Specifically, take an internet-social media break. Spend a few months with you.

Refrain from answering emails, logging into your social media networks, or reading articles about franchising-or business. Instead, spend some time away from your Smartphone. Maybe you can spend time outdoors, or at least somewhere that will provide a change of scenery. But, it has to be distraction-free.

Doing what I just recommended will force you to take a hard look at what you’re thinking of doing.

Summary

To sum things up, deciding to become the owner of a franchise business is a big decision. The preparation you do before you begin your franchise search really matters. That includes talking about your idea with your family, and spending a period of distraction-free time alone. Combined, all these action items will go a long way in preparing yourself up for success as the owner of a franchise.

When you are ready, please contact us

To sum things up, deciding to become the owner of a franchise business is a big decision. The preparation you do before you begin your franchise search really matters. That includes talking about your idea with your family, and spending a period of distraction-free time alone. Combined, all these action items will go a long way in preparing yourself up for success as the owner of a franchise.

When you are ready, please contact us

|  |

|  |

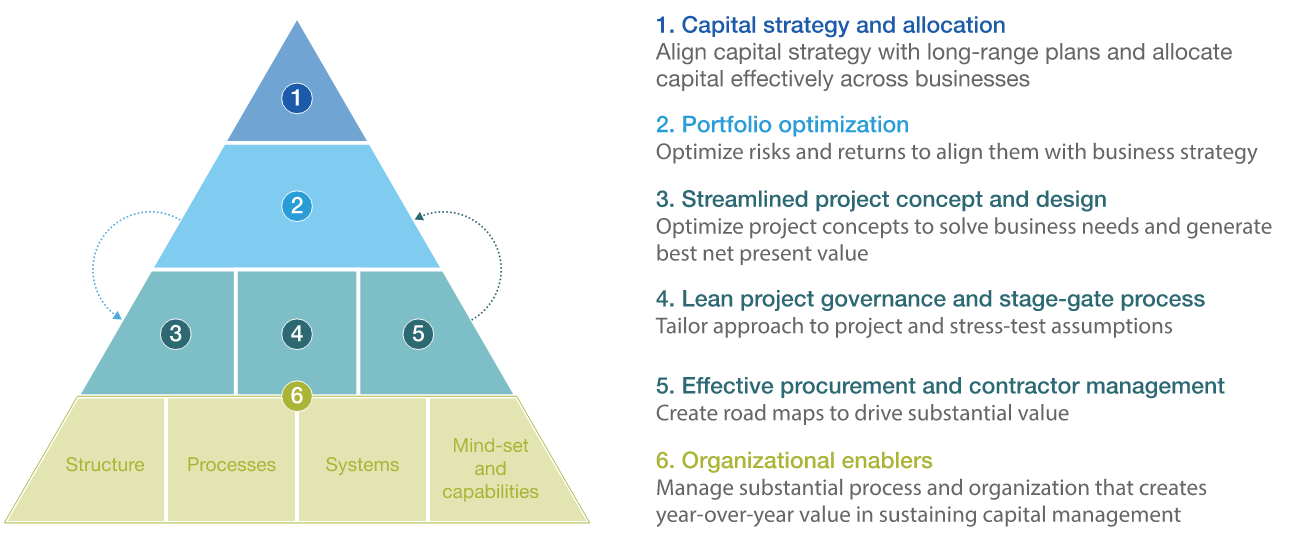

Managing smaller projects with increased rigor and a through-cycle mentality can help companies to capture significant untapped value.

Growth in the metals and mining sector typically requires large capital investments, which naturally garner considerable top-management attention. Yet these big projects account for only 50 to 60 percent of the sector’s $350 billion in annual capital spending. Many companies struggle to manage another category of capital expenditure with sufficient rigor: small investments to maintain existing assets, as well as small and midsize growth projects. And therein lies an opportunity.

Projects with a value of $50 million or less (frequently less than $10 million) make up a significant portion of capital spending for mining and metals companies: these projects typically account for 80 percent of all capital projects by number, and up to 50 percent of capital spending value. Yet many of these projects fall below the executive radar. According to the CFO of a diversified mining company, “We have a very solid central process to align capital allocation with corporate strategy, but [we are] primarily focused on major projects while the individual mines have a lot of autonomy in planning small capital projects.” As a result, these small projects can contribute to low investor returns. For example, the return on invested capital in metals and mining companies averages just 4 percent—typically below the cost of capital and much lower than the typical small-to-medium project, which have pay-back periods of less than 3 years.

But that’s just part of the equation. As demand for basic materials decreases, metals and mining companies dramatically reduce their capital investment; the industry reduced its capital expenditure (capex) by more than 25 percent between 2012 and 2016. The CFO of an international mining company recently confirmed that “in downtimes, we strictly limit capital allocation to safety and production, and reduce in-house project execution capabilities to reduce costs.”

However, we have found that decreases in capital spending rarely come with additional on spending (i.e., more robust processes to plan and manage small and medium capex). As a result, companies miss out on capturing additional value when demand returns—an opportunity they could seize by developing a through-cycle mentality to capex and increasing spend discipline.

However, we have found that decreases in capital spending rarely come with additional on spending (i.e., more robust processes to plan and manage small and medium capex). As a result, companies miss out on capturing additional value when demand returns—an opportunity they could seize by developing a through-cycle mentality to capex and increasing spend discipline.

Small and medium capex challenge

In dealing with small and medium capex projects, mining and metals companies face the following specific challenges:

- Time-force approvals. Management teams are asked for hundreds of approvals every year during the budgeting cycle.

- Weak business cases and risk assessment. Many business cases are poor or nonexistent, with no clear benefits or revenue impacts, underestimated costs, and optimistic schedules. Risks are not fully assessed and mitigation plans are insufficiently robust, leading to delays and cost overruns.

- Bundling of small projects into large packages. Many projects are bundled together under one large topic, and decisions are made for the entire package. Limited granularity means that low-return projects end up being approved.

- Poor tracking. Executives frequently lack transparency into real-time project progress, preventing timely management intervention.

- No feedback loop. Most companies do not have a structured review process, which inhibits future opportunities to learn from mistakes.

- Low productivity. Construction productivity often falls short; there is not enough true lean construction/execution.

Project sponsors are often overburdened and may lack time or technical capabilities to effectively stress-test proposed small and medium projects.

We observe mixed approaches among mining and metals executives when it comes to planning and managing small and medium capex. Some confirm that the prioritization process is “nonexistent” and that capex budgets are defined from the top down. “We do not have a specific process for prioritizing small and medium capex,” affirmed an international mining company CFO. Others describe a structured process in which projects are selected based on business logic, designed with optimal scope, and executed under stringent timelines with sufficient internal and supplier engagement. In many cases, these companies have robust stage-gate governance frameworks with clear requirements in place that would, if followed, lead to well-designed and executed capital projects.

The reality of the industry, however, is often different. Many companies overestimate returns, basing decisions on inconsistent assumptions or relying on unclear criteria for prioritizing small and medium projects. Project sponsors are often overburdened and may lack time or technical capabilities to effectively stress-test proposed small and medium projects. As a result, many of these projects do not generate the expected value or end up being relegated during the final approval process.

Implementing best practice

Best-in-class companies and executives overcome these problems by developing small-to-midsize capital-management dedicated programs and teams around six core building blocks: aligning capital strategy and allocation with corporate strategy; optimizing portfolios; streamlining project concept and design; implementing lean project governance; implementing effective procurement and contractor-management processes; and instituting sustainable organizational enablers (exhibit). In doing so, we have observed that they can deliver 15 percent to 30 percent additional value by improving the way they select and manage small-to-midsize projects.

Align capital strategy and allocation with corporate strategy

To achieve desired outcomes, mining and metals companies must translate overall corporate strategy into individual business-unit, regional and then mine/asset strategy, taking into consideration the risk-return profile of each entity. Best-practice companies ensure that projects are properly aligned with their overall strategy and are appropriately prioritized. Most recently, those companies are also incorporating lessons from the last few years and using a through-cycle mentality to determine optimal annual expenditure levels. Because many projects are small, the allocation is often made at the business-unit or even mine/asset level, which requires companies to adopt disciplined processes to ensure that expenditures align in the aggregate.

Leading companies in the industry also examine projects in terms of the value they create for the company overall, not only for the mine/asset. Often, this approach leads to the conclusion that a project should not be approved and that the value-creation goal can be achieved in other ways. This process also constitutes an important release mechanism, enabling companies to escape from the “engineer’s mind-set”—a focus on implementing the best engineered solution regardless of value. In addition, best practices also call for establishing systems to regularly monitor capital spending.

Optimize portfolios

Management teams often lack the data or processes to evaluate the merits of one project portfolio over another. Instead, they may pursue a default basket of projects year after year or make blunt, across-the-board spending cuts without actively shaping the portfolio for optimized growth and operations maintenance. In contrast, the most successful companies identify an optimal portfolio of projects, basing their assessment on two main factors:

Management teams often lack the data or processes to evaluate the merits of one project portfolio over another. Instead, they may pursue a default basket of projects year after year or make blunt, across-the-board spending cuts without actively shaping the portfolio for optimized growth and operations maintenance. In contrast, the most successful companies identify an optimal portfolio of projects, basing their assessment on two main factors: