This means that you can put a 25% down payment on a one-million dollar net lease commercial real estate property, and enjoy all of its monthly fixed income. Discover more of net lease commercial real estate, NNN-CRE, please visit our net lease commercial real estate Our recommended 5-year blueprint for you to build durable wealth. Below is how you can turn your $100,000 into $300,000 in five years, and create passive monthly income along the way. Please note if you do not have $100,000, you need to find a partner or investor who would joint venture with you. Other hand, if you already have $300,000, you can skip to the paragraphs after step #5. If you decide and desire, you can even turn your $100,000 into a cash-flowing million-dollar net lease commercial real estate in just five years: 1. Invest $100,000 by making five 20% down payments on five $100,000 turnkey cash-flowing single family properties. If you don’t know where or how, sign-up for our free 30-minute confidential consultant (link: https://www.dajkgroup.com/consultant--concierge-services.html). Do your due diligence. 2. Real estate has a historic appreciation rate of 6%. Compounded, each of your $100,000 properties is worth $134,000 within five years. That is $34,000 of appreciation in each of your five properties. Important Notes: Equity is the difference between what a property is worth and how much is owed on that property’s loan. Equity can also be thought of as your “skin in the game.” Cash flow is your monthly rent income minus mortgage, property taxes, property insurance, maintenance, professional management, and a factor for vacancy. It is your passive income. 3. So now for each property, you have $20,000 of original equity as the down payment, plus the $34,000 in equity from appreciation. That is approximate $54,000 in equity each property. 4. In fact, your tenant is also paying down your loan for you every month for five years. At today’s interest rates, that another $6,000 to add to your $54,000. That’s a grand total of $60,000 of equity for each property over five years! 5. That $300,000 of total equity over your five rental properties, it is just five years after you began with $100,000. It’s the magic of financial leverage coupling with a compound interest at work. You achieved the rate of appreciation on both your down payment and the money that you borrowed from the bank. Compound interest is slow, lame; and it doesn’t create wealth on its own. Wealth is created when compound interest is leveraged this way. After five years’ time, you can keep holding your five properties, exchange via 1031 (tax deferred strategy) or sell them and cash in. For example, you decide to sell your five properties. You won’t get $300,000 in equity cashed out. When you pay agent commissions and property make-ready costs, it might get whittled to $250,000. With your $250,000, you typically do not have to pay any tax (yes, zero tax) on your capital gain if you use it as a down payment for another property (follow the generous tax-deferred exchange rules). This means that you can put a 25% down payment on a one-million dollar net lease commercial real estate property, and enjoy all of its monthly fixed income. Discover more of net lease commercial real estate, NNN-CRE, please visit our net lease commercial real estate (https://www.dajkgroup.com/net-lease-investment.html ) Yes, now you’ve created financial leverage on an even larger property and continue to amplify your wealth in the same way! Intrigued? This experience also means you understand some risks and limits. The above example is surely simplified. What’s are some risks and limits?

Please note real estate pays you five ways at the same time. In growing $100,000 to $300,000 in five years, we’ve only discussed two of just five ways you’re paid with residential, cash-flowing real estate! Those two are appreciation and mortgage pay-down made by tenants. There’s also cash flow, tax benefits, and inflation-hedging. Please note a structuring with a lease option investment property, tenant/future owner manages the property for you. Your time is worth too much to replace flooring, fix faucets, or collect rents yourself. Be an investor! This is about smartly investing your money over time to leverage other people’s money to build durable, lasting wealth for you and your future. I encourage you taking action. Please sign-up for our free 30-minute confidential consultant. Strategically and Smartly leverage your way to financial freedom.

1 Comment

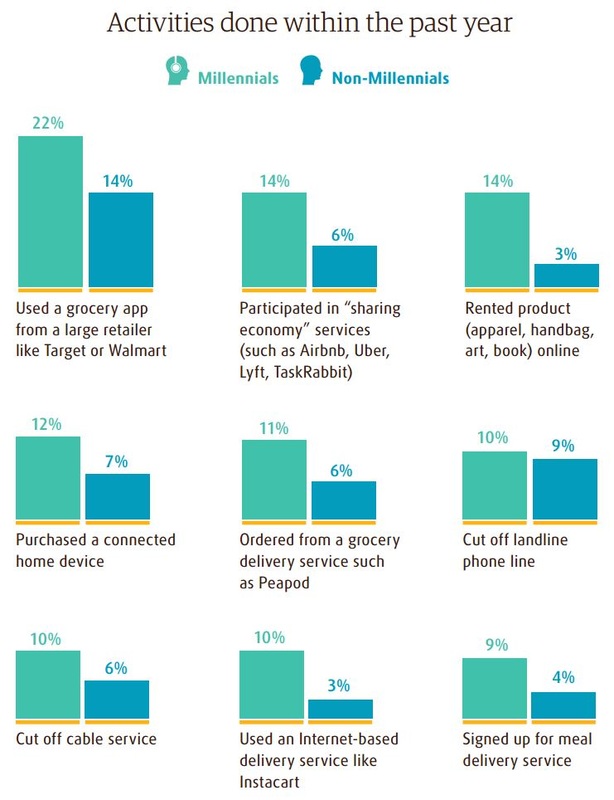

Millennial shoppers transforming retail Those retailers who can’t elevate their game won’t be on the playing field for long  While e-commerce presents new, unparalleled possibilities for accelerated growth, most retailers also are going through unprecedented challenges, and their very survival is in query. They must preserve with ever-evolving science and client expectations. Also omnichannel retailers are being pushed via patrons to give a compelling, seamless experience across all channels. The traces of big difference between brick-and-mortar and digital experiences are endlessly blurred. Retailers of all sizes are experiencing tensions within their organization about prioritizing the alterations wanted to remain aggressive. The insights provided listed here are designed to aid them check the exceptional path ahead as they navigate the intricacies of a market that is in no way been tougher. They are clearly divided into four categories:

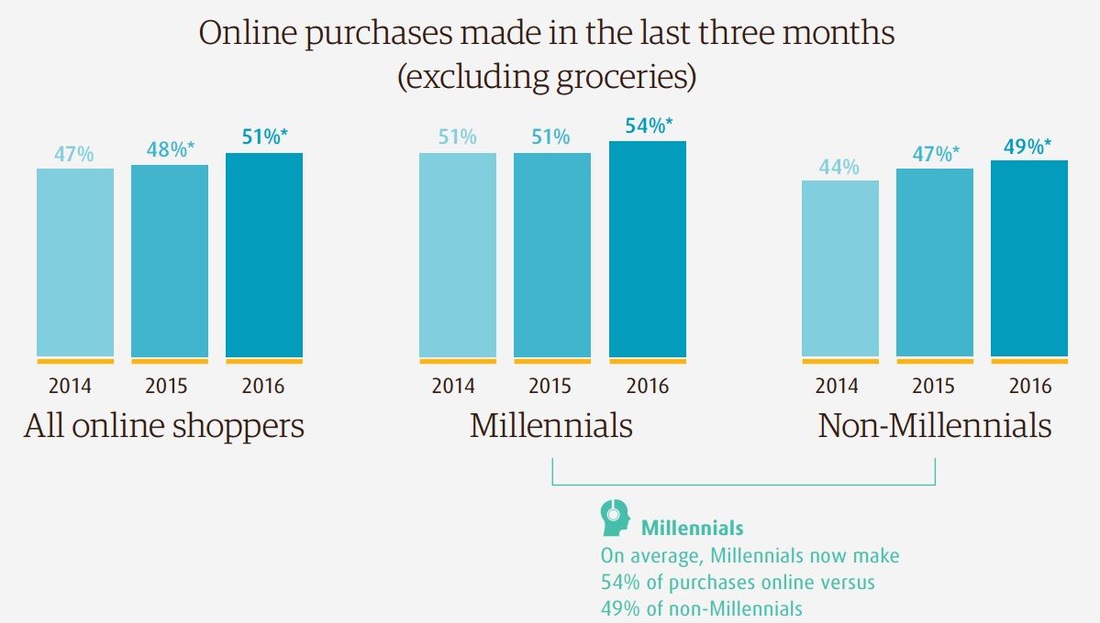

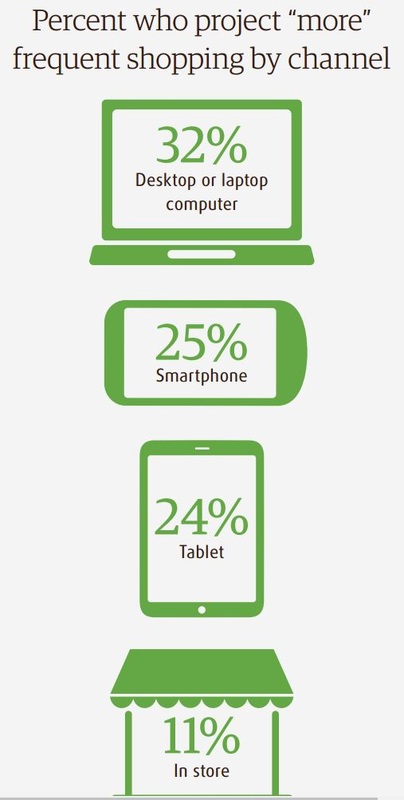

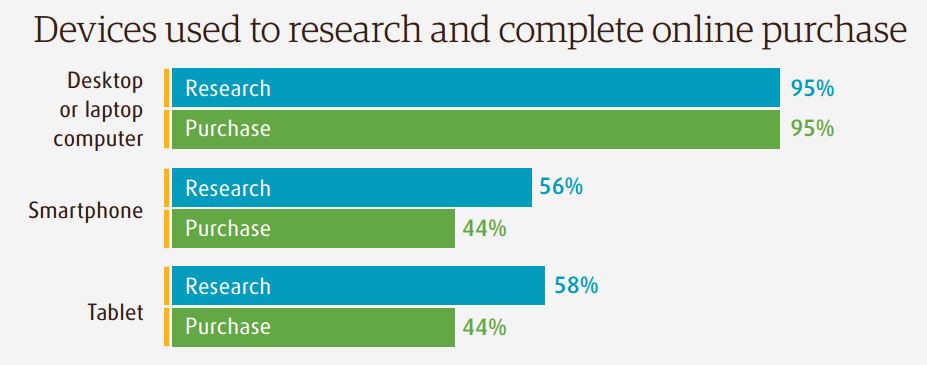

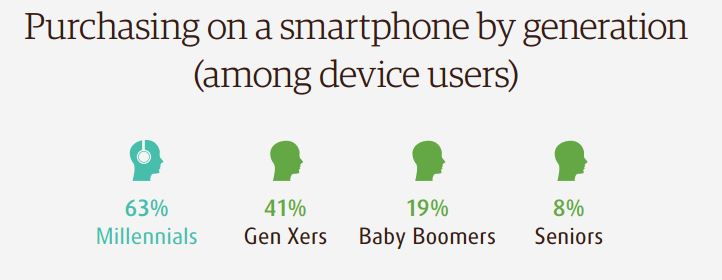

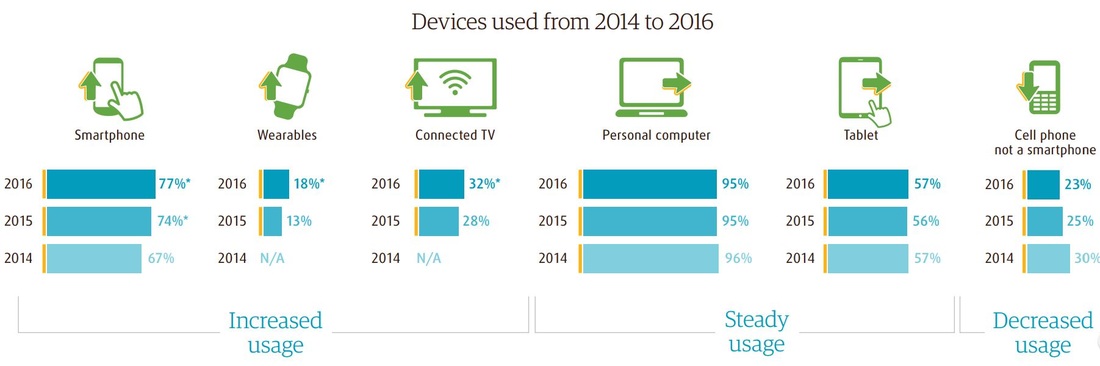

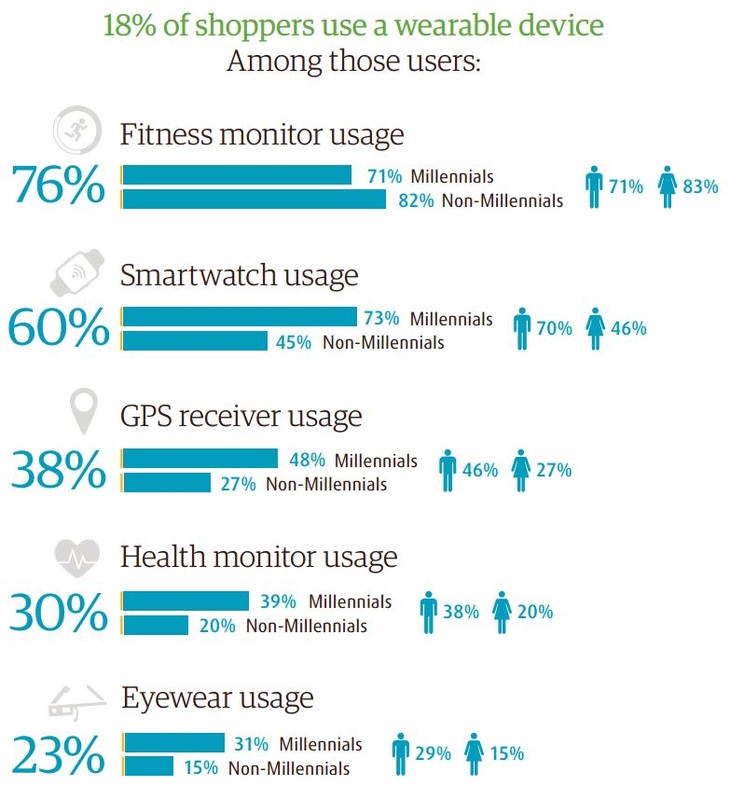

Shoppers are shifting transactions to digital For the first time, online shoppers in this survey now state that on average just over half of their purchases were made online. Increase in use of digital tools projected While the PC remains a stalwart, one in four shoppers are projecting more shopping on smartphones and tablets. Since 2014, user intentions to shop more have increased each year for both PCs and smartphones.   Mobile means business Purchasing on mobile is increasing, so retailers must continue to optimize their online experience via these devices. The study shows that customers are often using their smartphone as the glue that connects all shopping interactions — from PC to tablet to store.   Millennial technology behavior a disruptor Millennials are adopting devices and participating more in technology services overall, including shopping-related activities, resulting in consumer behavior shifts that have implications for all retailers. These “tech natives” will become even more prevalent in years to come  Device adoption rates telling A three-year comparison of adoption rates among online shoppers reveals that many new technologies — including smartphones, connected TVs and wearables — are up. Adoption rates of personal computers and tablets are stable.  Wearables interest strongest with males and Millennials Manufacturers are investing heavily in wearables. Global analyst MarketsandMarkets estimates that this sector will grow from $23 billion today to $173 billion in 2020. Wearables use is up 5% from 2015 to 2016 and varies by age and gender.  Product searches usually don’t start with search engines Contrary to findings from other sources, the avid online shoppers in this survey started just 15% of their product searches with Google, Bing, etc. Instead, product searches were started 35% of the time at marketplaces (27% Amazon and 8% others), 31% at retailers’ channels (14% website, 13% in store, 4% app), 6% with catalogs and circulars and 4% at a social network Source: UPS Research Please Click on Images Below for More Details...

The Brent crude oil price forecast for 2017 was increased by $1 per barrel from the November STEO, with 2017 prices expected to average $52 per barrel in the December STEO. Brent and WTI crude oil prices for the first half of 2017 are projected to remain near $50 per barrel, with prices ending the year around $55 per barrel. Crude oil Prices: Crude oil prices traded below October levels for most of November before increasing significantly on the last day of the month. West Texas Intermediate (WTI) crude oil prices increased from $46.67 per barrel (b) on November 1 to $51.06/b on December 1, while international benchmark Brent crude oil increased by $5.80/b over the same period to settle at $53.94/b. WTI and Brent average spot prices in November were $4.07/b and $4.79/b lower, respectively, than the October averages. At their November 30 meeting, members of the Organization of the Petroleum Exporting Countries (OPEC) announced a framework for supply reductions among most of its members. Several non-OPEC producers also announced their intention to freeze or reduce production. The extent to which the announced plans will be carried out and actually reduce supply below levels that would have occurred in their absence remains uncertain. If the agreement contributes to prices rising above $50/b in the coming months, it could encourage a return to supply growth in U.S. tight oil more quickly than currently expected. Crude oil prices near $50/b have led to increased investment by some U.S. production companies, particularly in the Permian Basin. A price recovery above $50/b could contribute to supply growth in other U.S. tight oil regions and in other non-OPEC producing countries that do not participate in the OPEC led supply reductions. Continuing global supply growth in 2017 may postpone significant global inventory withdrawals until 2018, with the first half of 2017 showing inventory builds averaging 0.8 million b/d in our current forecast. Global inventory builds are forecast to average 0.4 million b/d for all of 2017. Despite new oil production coming online when oil inventories are at high levels globally, global economic data have been more positive than previous expectations, and increases in oil demand growth could help to support prices in the coming quarters. The Brent crude oil price forecast for 2017 was increased by $1/b from the November STEO, with 2017 prices expected to average $52/b in the December STEO. Brent and WTI crude oil prices for the first half of 2017 are projected to remain near $50/b, with prices ending the year around $55/b. Implied volatility increased in the weeks prior to the OPEC meeting, suggesting significant uncertainty regarding both the prospects for the recent agreement and its potential implications for global oil balances. Oil production, particularly in the United States, has been more resilient in the current oil price environment than had been expected, as reflected in improving financial conditions at oil companies. Improved profits could encourage oil producers to increase capital expenditures and expand production in 2017 and beyond, especially if oil prices increase. In the third quarter of 2016, a group of publicly traded global oil companies reported the first quarterly profit from upstream production business segments since the fourth quarter of 2014, according to recently released earnings statements from 91 companies. Collectively, the group earned almost $2.3 billion in the third quarter when front-month Brent crude oil prices averaged $47/b. In the same period in 2015, when prices averaged $51/b, the group lost $54.1 billion. Since the fourth quarter of 2014, many companies have written down the value of their assets to reflect lower oil prices, which reduces earnings in the quarter in which a company recognizes the write-down. The increase in earnings this year is partially attributable to a reduction in asset write-downs, which declined 80% year-over-year. Additionally, company reductions in operating expenses were greater than the declines in revenue, contributing to higher profitability. One example of an impairment charge is Royal Dutch Shell's announcement to discontinue a Canadian oil sands project, reducing its proved reserves by an estimated 418 million barrels, according to company filings. A different company, Whiting Petroleum, wrote down the value of some assets it acquired from Kodiak Oil and Gas when the two companies merged last year. Large impairment charges represent acknowledgement by a company that some of its projects are no longer profitable and are being discontinued. While this adjustment reduces the investment expenditures that the company would incur, it also reduces the future estimated cash flow from these projects. Options for conserving cash include reductions in dividends to shareholders, elimination of share repurchase programs or increases in cash through share issuance, increasing debt, or sales of assets. Since 2014, these 46 companies reduced dividends by 16% and share repurchases by 92%. Impairments make increasing debt and selling assets more difficult. Lenders may be less willing to lend if a company's assets declined in value, or may only be willing to lend up to a certain percentage of the value of a company's proved reserves, which declined in value from impairments. Selling assets becomes difficult because they are typically sold at a lower valuation than when the company purchased them because of the impairment charge, raising less cash than otherwise would be expected. Full e-report STEO December 2016 will be emailed to you upon receipt of your request with our contact. Source: US EIA Click on these images below for further details

Last week oil prices suffered their fourth losing week in a row as OPEC continued to argue over a possible production freeze/cut and oil production continued to grow adding to the surplus. At week’s end, futures prices were down to $43.41 in New York and $44.75 in London. The surprising US election results roiled for a few hours on after the results became known, but prices settled on Wednesday with a small gain and were down on Thursday and Friday on new reports of oil production increases and stockpile builds.

OPEC officials continue to maintain that the organization and Russia are committed to the Algiers deal, but most traders and hedge fund managers became skeptical after the failure of the October 28th meeting in Vienna to work out the details. With the exception of the OPEC hype, most of the news last week was bad for prices. The EIA reported another build in US crude stocks; money managers slashed long positions in crude; the EIA reported that the global oil supply rose by 800,000 b/d last month; and that the global market will be awash in oil next year unless OPEC makes significant cuts. The Agency raised its forecast for non-OPEC production increases next year to 500,000 b/d with the increase coming from Russia, Brazil, and Kazakhstan. On Friday, Iran announced that its oil production had increased by 210,000 b/d last month to 3.92 million. This was the biggest monthly increase since the end of the sanctions and 230,000 b/d more than OPEC’s estimate of Iranian production in October. Most observers see the major Middle Eastern producers jockeying for position ahead of the OPEC meeting at the end of November. Another indication of a growing glut was a report that European oil companies have been forced to book oil tankers to store their growing oil supplies as there is no longer any room left on land. There are now 14 to 16 600,000-barrel tankers storing crude in the region, and more are scheduled to be loaded in November. Some are predicting that oil prices will fall into the low $30s or worse if the upcoming OPEC meeting is a failure. In the longer run, however, the likelihood that Venezuelan oil production will continue to shrink and the continuing drop in major oil company capital expenditures is likely to eat away at overproduction even if US shale oil production rebounds. 2. The Middle East & North AfricaIran: Tanker trackers confirm that Tehran’s claim that it increased production by 210,000 b/d last month to 3.92 million b/d is probably true. The Iranians say they too are optimistic that an OPEC oil production agreement will be signed, but still maintain that they are exempt so that the Saudis and others can do the freezing. The big Iranian oil story last week was that France’s Total signed an agreement with Iran to develop part of the South Pars natural gas field. The deal, which may ultimately be worth some $6 billion, is the first post-sanctions agreement signed with the Iranians since the sanctions were lifted. Total had started work on the South Pars field but withdrew from the project six years ago amid rising tensions over Tehran’s nuclear ambitions. For the French, the agreement was simply a renegotiation of a project that they began working on many years ago. China’s National Petroleum Corp also is set to sign a deal to develop the South Pars field. South Pars is shared with Qatar, which is already exploiting its portion of the field. The Iranians fear that the Qataris might be able to produce more than their fair share of the gas, so they are eager to increase production. Like other Middle Eastern countries, Iran is working on laws to spur renewable energy investments, including wind, solar, and hydro projects. Like the Saudis and others, dependence on oil and gas for the bulk of its energy is not only a more expensive way to produce electrical energy, but they have to look forward to the day where production will run dry or be curtailed by climate change agreements. Egypt’s oil minister was reported to be in Tehran last week after the Saudis stopped oil shipments to Cairo. Tehran denies that any agreement to replace the Saudis has been reached. Tehran must be concerned about some of the campaign rhetoric coming out of the recent US elections. President-elect Trump said numerous times that as President he would tear up the nuclear agreement and bring the Iranians to heel by using military force. Given that the EU, Russia, and China are satisfied with the agreement, the impact of a unilateral US pullout would be limited if Tehran’s frozen assets already have been returned and the US has only very limited economic relations with Iran. US Republicans are refusing to lift the remaining sanctions on Iran as Tehran continues missile tests, behaves aggressively in the Gulf, and jails US citizens. A tougher line from Washington, however, could damage the Rouhani government which is already walking a thin line in signing the nuclear agreement. Should the agreement break down, Iran would likely seek to strengthen its relationship with Moscow. Syria/Iraq: There is little going on in Syria these days which directly affects Middle Eastern oil production. The US and various allies, including Iraqi Kurdistan, are preparing for an eventual assault on ISIL’s capital of Raqqa. Meanwhile, the many-sided struggle for Aleppo continues with ever-increasing casualties. The only thing that is certain is that there will not be much left of Syria when the civil war finally ends. There was some oil news from Iraq last week. Kurdistan oil revenues were up in October, but still not high enough to meet the government’s needs in conducting the war against ISIL. The Iraqi Oil Ministry, which had announced plans last month to contract for the development of 12 small oil fields to foreign oil companies, announced that those plans had been changed. State oil companies will develop some of the fields and rest of the plan has been delayed until the middle of next year. The Oil Ministry is scaling back on plans to build a massive water injection system in Southern Iraq. Water flooding of Iraq’s aging field is seen as the best way to maintain and increase oil production in the region. The revised project is much smaller in scope making it more affordable to implement in the short term. A smaller water-flooding system would delay plans to increase oil production to much higher levels. Saudi Arabia: Riyadh told Cairo last week that it was halting deliveries of oil products under a $23 billion aid agreement. Although the Saudis deny it, the reason for the move is thought to be Egypt’s refusal to support the Saudis in a UN vote on the situation in Aleppo. There are indications that Egypt may be turning to Iran to replace the Saudis as the key supplier of oil. There are still no definitive announcements as to the Saudis’ position on the OPEC production freeze. The most we have heard is that Riyadh and its Gulf allies will not be the only ones to bear the burden of production cuts. Low oil prices are continuing to take a toll on the Saudi economy. The government has canceled some $266 billion in planned and ongoing construction projects. The government’s unpaid bills owed to construction firms, medical establishments, and foreign consultants have burgeoned during the financial crisis. One analyst estimates that the government owes construction firms alone some $21 billion dollars. The oil price slump created a $98 billion deficit last year and the deficit in 2016 is expected to be around $87 billion despite a recent $17 billion bond issue. The cutback in construction has resulted in the laying off of some 70,000, mostly foreign, workers and there are tens of thousands of layoffs to come. Many government contractors are going into bankruptcy for lack of government payments. Most of the burden is falling on foreign workers, who are being sent home as contracts are ended. The Saudis are eating their way through their sovereign wealth funds at a pace that will leave them in big trouble in four or five years unless oil prices recover. Libya: The country’s largest oil export terminal, Es Sider, may resume shipment this week as maintenance work nears completion. The terminal has not exported any oil for the last two years. Libya is currently producing about 660,000 b/d and claims to be able to produce close to 1 million if the terminals are open. Before the uprising, the country was producing 1.6 million b/d. 3. ChinaBeijing’s crude imports in October fell by 12.9 percent from the record high in September to 6.78 million b/d -- the lowest level of imports since January. China’s domestic production in October was down, suggesting that domestic consumption was lower than usual. During the month, China’s exports of diesel and gasoline jumped by 24 percent year over year to 919,000 b/d as Chinese refiners produced more finished products than the economy can absorb. China’s October imports, however, were still 9.3 percent higher than in October 2015. As usual, there still is not a good fix on how much of China’s oil is going into strategic storage. The bottom line is that there is still an oversupply of crude in Asia despite analysts’ hopes that the supply/demand gap would be closed by now. Much of the energy news from China last week concerned coal and Beijing’s efforts to clean up its air by cutting production. Coal production has dropped in the last two years as the government closed many small and inefficient mines. It now appears that they have overdone the cuts and have been forced to import increasing amounts of foreign coal to keep their power plants burning. Imports of coal from Australia jumped 33 percent in the 3rd quarter and have led to a marked rise in coal prices. This, in turn, has led to government efforts to lower coal prices by manipulating the prices that large state-owned coal mines receive for their coal. Some are concerned that China’s efforts to become a world leader in setting commodity prices is being bungled by the coal situation. Beijing has reacted with unusual vigor in warning President-elect Trump of the consequences to the planet if he succeeds in slowing progress or even torpedoing the recent climate change agreement. Former President Bush did much the same thing with the Kyoto agreement 15 years ago. For a long time, China resisted whole-hearted participation in efforts to control emissions until dangerous levels of pollution began enveloping its major cities and giant typhoons began battering its coasts. So far the Chinese now are feeling the effects from decades of minimal pollution controls and the early years of global warming far more than dirty air and climate change is hitting the US. India now fears that should the US pull out of the Paris agreement, other countries will follow. Beijing says it will carry on with its plans to reduce emissions no matter what the US does. Source: Oil Review and EIA

ERA will begin accepting submissions Oct. 28, 2016 and submissions close Dec. 15, 2016. Emissions Reduction Alberta (ERA) is making up to $40 million CDN available to advance technologies that address methane detection, methane quantification or reduce methane emissions in Alberta. There is a maximum of $5 million per project and up to 50% of eligible costs. ERA is the new tradename of the Climate Change and Emissions Management (CCEMC) Corporation. We were established as a key partner of the Government of Alberta to address climate leadership priorities. ERA will begin accepting submissions Oct. 28, 2016 and submissions close Dec. 15, 2016. Projects can include prototype development and testing, field pilot projects and demonstration projects. Ideas can come from anywhere, but all projects must demonstrate a clear and justified value proposition for addressing methane emissions in Alberta. Field pilots and demonstration projects must occur in Alberta. Multiple-site pilot and demonstration projects are eligible. We are seeking projects that reduce methane emissions from across Alberta’s sectors, including: • Agriculture • Mining • Oil and gas • Waste management The size of opportunity and potential for widespread methane reductions will be taken into consideration during ERA’s evaluation and project selection. WHY METHANE? The climate change impact of methane is significant — 25 times greater than carbon dioxide over a 100-year period. The Alberta Climate Leadership Plan aims to reduce methane emissions by 45% by 2025. ERA is well positioned to play a role in supporting medium- and longer-term methane emissions reduction. The oil and gas industry is responsible for 70% of Alberta’s methane emissions. 31.4 megatonnes in 2014

12.5 megatonnes in 2014 Please contact us for further information if you are interested.

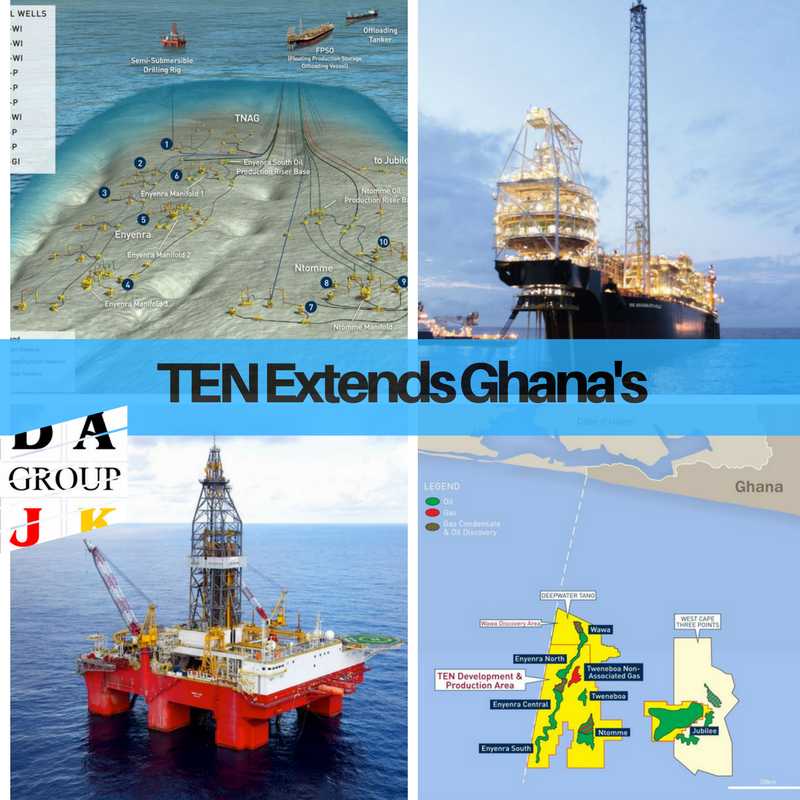

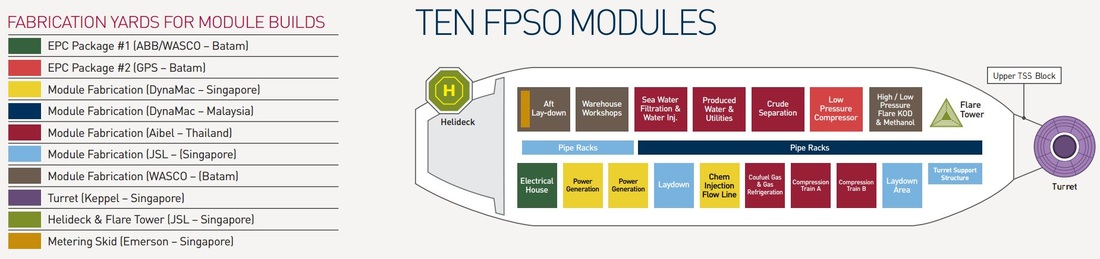

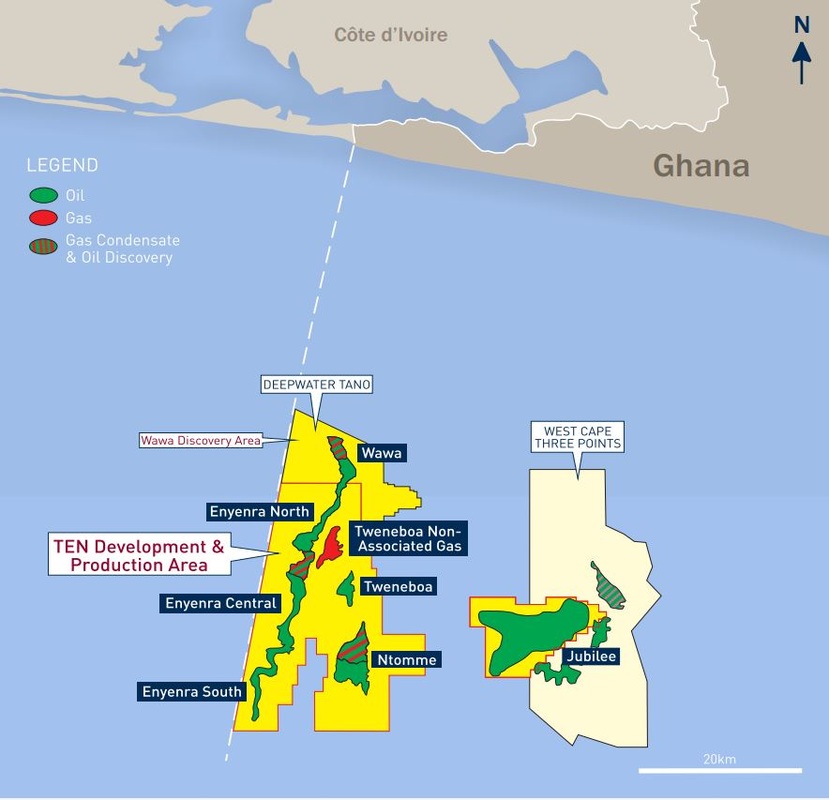

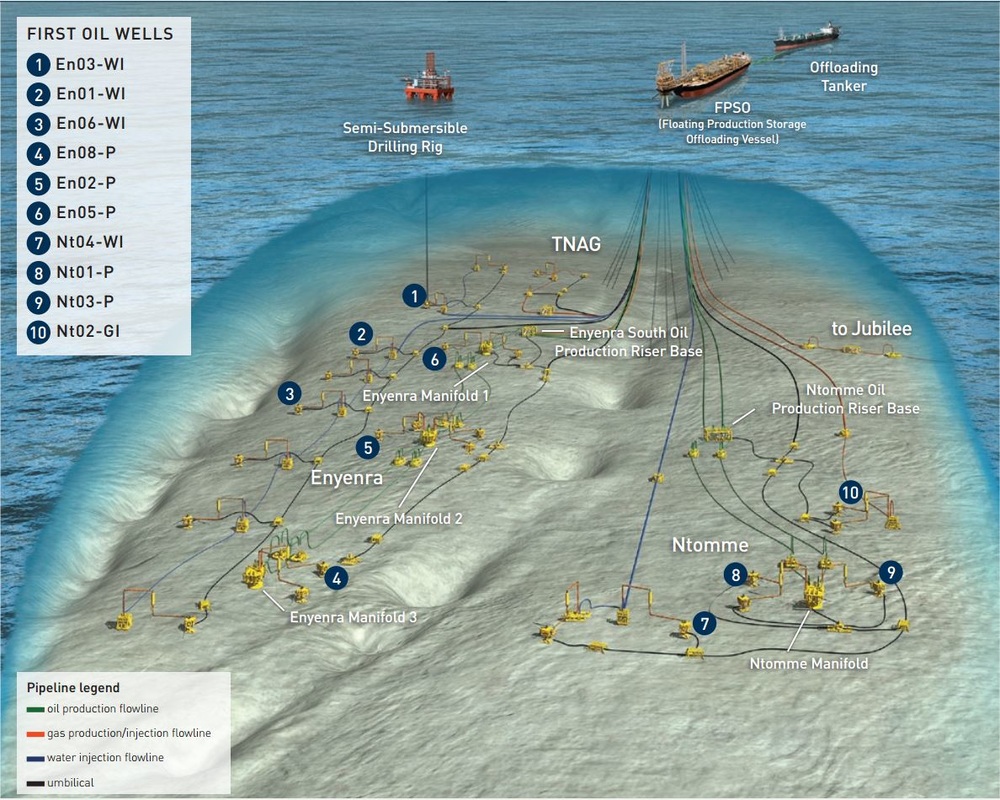

TWENNEBOA, ENYENRA & NTOMME (“TEN”)The TEN Fields lie in the Deepwater Tano block, around 60 kilometres offshore Western Ghana. The fields are spread across an area of more than 500 square kilometres, around 20 kilometres to the west of the Tullow operated Jubilee Field. The reservoirs lie in water depths ranging from 1,000 to 2,000 metres. Following the discovery and appraisal of the fields, the TEN Plan of Development (PoD) was approved by the Government of Ghana in May 2013. The full field development will consist of 24 wells in total – a mixture of water injection, gas injection and production wells which will all be connected to the FPSO through subsea infrastructure. Ten wells were required for First Oil and have all been drilled. The project tendered its major contracts shortly after PoD approval and all key awards were made by September 2013. The conversion of the FPSO began in October 2013, with the arrival of the Centennial Jewel tanker in Singapore. The installation of the subsea umbilicals, risers and flowlines began in July 2015 and lasted almost exactly one year. After nearly 28 million man hours of work the project delivered First Oil on schedule in August 2016.   Ghana’s second deepwater development has come onstream within budget, just over three years after the government sanctioned the project. The TEN project in the Deepwater Tano license covers three fields in water depths of 1,000-2,000 m (3,281-6,562 ft), 20 km (12.4 mi) west of the Jubilee field. Operator Tullow Oil, in partnership with Anadarko, Kosmos Energy, Ghanaian National Petroleum Corp. (GNPC), and PetroSA, commissioned MODEC to convert the double-hulled VLCC Centennial J into the 340-m (1,115-ft) long, 56-m (184-ft) wide FPSO Prof. John Evans Atta Mills. The FPSO, moored in 1,500 m (4,921 ft) of water, is designed to process up to 80,000 b/d of oil and 180 MMcf/d of gas. It is connected via subsea manifolds, flexible flowlines and static/dynamic umbilicals to oil and gas production wells and water and gas injectors - depending on performance and future plans, up to 24 development wells may eventually be drilled. Tullow anticipates a productive lifespan of 20 years. Project manager Terry Hughes spoke to Offshore about the various issues the partners dealt with along the way, including reservoir depletion mechanisms, managing engineering, lessons learned from Jubilee, and local content. Offshore: This is Tullow’s first experience of overseeing development of a major deepwater project. How has the company approached this task? Hughes: I joined Tullow in 2011 specifically for TEN, having previously worked with several upstream operating companies doing major projects offshore and onshore around the world. I joined towards the end of the concept selection phase which had concluded TEN was best developed using an FPSO and subsea infrastructure. We then formed a team to complete the technical and engineering requirements from all areas - subsurface, wells, subsea, facilities etc - needed to make a well defined proposal to the field partners to proceed with the development. That was done by early 2013 and TEN completed its sanction and received government approvals in May that year. The next step was to execute the sanctioned project and the team was put in place to do this. With Jubilee, Tullow concentrated on preparing for the operating phase after the major project phase was completed. The project phase itself was executed by an integrated project team drawing expertise from all the partners, led by Kosmos Energy. Several Tullow employees were part of this team, but Tullow’s focus was preparing for operations, which meant assembling a significant group of people, mainly based in Ghana, to oversee field operations. Tullow took all that experience and knowledge into the TEN Project which was a significant step up in size and scale.  Location of the TEN fields offshore Ghana. (All images courtesy Tullow Oil) In the project’s early phase, our main partners, Anadarko, Kosmos and GNPC, had a lot of engagement with Tullow as they wanted to understand and provide input into our execution plan and the building up of our team. As the project progressed on schedule and on budget, I believe they became increasingly confident in our capabilities, allowing them to step back a little. Offshore: The exploration campaign that led to the three TEN discoveries on the Deepwater Tano block took place during 2009-12. What is your resultant understanding of these structures and their characteristics? Hughes: The acreage was covered by spec 3D seismic that had been acquired in 2000. We call TEN ‘the field,’ although it actually comprises various reservoirs in different formations - Tweneboa, Enyenra, and Ntomme are various rock types. We have also procured seismic outside the areas where oil and gas has been found in order to correlate the data better, and to look at opportunities for future tie-ins. Certainly, 3D seismic provides a lot more definition and helps to fine-tune the bottomhole locations. And combining the 3D data with the well results allowed us to optimize our development plan, including the reservoir depletion mechanisms. We now know, for instance, that one field features a gas cap and water drive rather than just being a gas-drive field and we have modified our depletion plans in response. As for our predictions on reservoir behavior, you might say we are currently in the middle of the uncertainty range. But once we obtain production history and see how the wells behave, we are hopeful the volume of recoverable reserves will increase. So far all the wells have come in on target, most with slightly better quality reservoirs than we predicted. For several years we have installed pressure gauges in our wells, enabling us to monitor the pressure pulses in the reservoirs which gives our engineers valuable insight into how the reservoirs will behave. It all looks good but we really need some production history to correlate our models and then we can update our predictions. The main reserves, and consequently our focus for the early part of the development, are in the Enyenra and Ntomme reservoirs. Most of TEN’s producing and injecting wells have been drilled on these structures which make up the bulk of the 300 MMboe we believe are recoverable. We are only developing one pocket of the reservoirs at Tweneboa, which is a gas field, and this is not due to start production until mid-2018. The depletion plan for the three fields differs: Tweneboa is via gas condensate blow down; Enyenra - pattern waterflood; and Ntomme - crestal gas injection and flank waterflood driven by reservoir geometry and fluids. Production rates per oil producer across the fields are variable, in the 10-15,000 b/d range. This was confirmed during short flowback tests when we were installing production tubing strings into the wells. Offshore: The 2009-12 campaign also led to discovery of the Okure, Oyo, Sapele and Wawa fields - why were these excluded from the current development? Hughes: Our approved plan is to execute TEN as I have described which includes some pre-investment in the facilities to enable future developments and tie-ins to proceed efficiently. We are well placed now to evaluate options to extend the TEN plateau period or overall field life. We already have a team doing the early planning work and, when it’s complete, we will bring the options forward for our partners and the government of Ghana to consider.  Offshore: Various technical issues have cropped up at Jubilee since production started there, notably in the wells and more recently, the bearings in the FPSO’s turret mooring system. Were the partners looking to either replicate or avoid certain experiences from that project with TEN? Hughes: We had an extensive lessons learned initiative in TEN which sought to replicate all the things that went well on Jubilee and avoid some of the issues seen after a few years of its production history. The timeframe between the discovery of the Jubilee field and first oil was incredibly short. The integrated project team did an excellent job bringing that field into production quickly, which benefited all parties, but inevitably they had less time to refine and optimize designs and execution plans. Taking this lesson on board, for TEN we expended extra effort on front-end work in order to ensure we had the right design and that the execution plan was sound. I believe we found the right balance between engineering, design and execution - and with firm project management and rigorous management of change culture, we were able to deliver on time and on budget. There are lots of stories of projects going wrong in the execution phase following repeated alterations to their scope. Offshore: Government approval for the development came in 2013, shortly after the conclusion of exploratory drilling. This seems ultra fasttrack compared with other West African deepwater projects - was this due to the government’s keenness to develop the country’s oil and gas sector as quickly as possible. Hughes: TEN was not actually planned and executed as a fasttrack development. Tullow does not think or act like a major oil company - we are a smaller organization with a more manageable portfolio. With less internal competition for resources, we are able to bring focus and get things done in a shorter period. Clearly, we had to conduct significant exploration and appraisal on a field of this complexity and we spent nearly $1 billion on E&A. With such a significant investment to confirm the size of the resource, we were highly motivated to bring the project forward for sanction as quickly as possible and happily the government of Ghana was like-minded. Offshore: Was one of the government’s conditions for sanctioning the project stepping up involvement of Ghanaian nationals, or would the partners have done this anyway? Hughes: In both cases, yes. The partners would have done it for two reasons: firstly, in Tullow’s case, and probably the same applies to our partners, we have always pushed for local people and local industry to share the prosperity of major finds such as TEN. At the same time, the Ghanaian government and regulator have displayed equal drive to see increased local participation. For these reasons we asked each of our major contractors to include local content plans in their tenders and made them part of our contracts. For example, FMC Technologies, which was awarded the contract for the subsea production systems, has assembled and tested the subsea trees for TEN at their facility in Ghana which has a predominantly local workforce. Other examples are the new Sekondi fabrication yard we used with MODEC and Technip to build piles and structural components for TEN’s subsea architecture; and the Takoradi yard where Subsea 7 has manufactured a complex gas export manifold which will soon be installed on the seabed - a full year ahead of schedule. This will allow TEN’s gas to mix with Jubilee gas being exported to the Ghanaian shore. MODEC also used local companies to build components that were sent to Singapore and installed on the FPSO.  Seadrill’s semisubmersible West Leo has drilled and completed the first-phase TEN wells. Doing this work in-country builds capacity and enables knowledge transfer to Ghana. We supplemented these efforts with a secondment program which saw employees from the GNPC and Petroleum Commission of Ghana join our project teams in London, Singapore, Paris, and Houston to gain news skills and experience. Offshore: Did MODEC win the contract to supply the weather-vaning, turret-moored FPSO based partly on the partners’ experience working with the company on the Jubilee floater? Hughes: Clearly this formed part of our thinking, but they still had to go through the process of bidding. All bidders had to consider our requirements and enter a year-long design competition which required extensive engineering and planning work to support their bids. MODEC emerged successful from this process. After winning the contract, MODEC bought and converted a VLCC tanker in Singapore and the resultant FPSO Prof. John Evans Atta Mills, named after the late Ghanaian president who facilitated first oil from Jubilee, reached Ghana this March. It was then moored via nine chains connected to suction piles, all built in Ghana, at the TEN location. Intense planning was necessary to anchor the FPSO in the optimum position to connect to the extensive network of subsea equipment needed for the 24 wells that will ultimately be drilled in the field. On completion of the mooring and hook up of flowlines and controls, the vessel underwent an extensive commissioning and testing process. First oil was produced on Aug. 17. We will soon begin injecting associated gas into the Ntomme reservoir, and then next year gas export to the shore will begin. Offshore: Is development drilling on track? Hughes: All is on track with our plans for first oil. Our development plan is for a total of 24 wells, 10 of which were required, and will be delivered, by first oil. The well stock is a combination of re-used E&A wells and new wells. There is a maritime border dispute between the governments of Ghana and Côte d’Ivoire and until the resolution of this process, we cannot initiate any new drilling. However, we had already completed the drilling of our first oil wells when the drilling hiatus was imposed. The border dispute will be resolved by ITLOS [International Tribunal of the Law of the Sea] in 2017, after which we hope to resume our development plan. Though not ideal, this drilling hiatus does mean that when we resume drilling it will be at the lower rig rates we now see due to the change in market conditions experienced over the last year. Offshore: Will all the subsea equipment be in place before start-up? Hughes: Everything apart from the gas export manifold is in place, and we expect to install the manifold in September, nearly a year ahead of plan. FMC should deliver the last of the subsea trees next March, making them available for when we resume drilling. Our wells feature smart completions which allow us to monitor and control individual reservoir zones.  Offshore: Can you provide details of the production capacity and offtake arrangements? Hughes: The facilities can handle up to a nominal 80,000 b/d of oil, with storage capacity of 1.7 MMbbl. Every two weeks during the plateau period, one cargo of 1 MMbbl will leave the facility which is of similar oil quality to Jubilee. We are also hopeful that we will be ready to export gas in 2017 - much earlier than planned. Offshore: Following the oil price ‘shock,’ did the partners and the Petroleum Commission get together to find ways of bringing the project costs down? Hughes: Yes. When we sanctioned the project, our contracting strategy was to secure capacity and minimize risk and exposure. Some of that required ‘lump sum’ contracts where the price is fixed up front so we were limited in what we could do here. But where costs were not fixed, we have achieved some savings. We will not finalize our numbers for a little while yet, but our capital costs to first oil will come in under the $4-billion figure we approved at sanction. And of course, the TEN fields will be operating for many years to come so we are looking hard at our operating costs and the synergies we can achieve from a two-field operation. Offshore: Will Tullow have to relinquish any parts of the Deepwater Tano license at some point, including any of the discoveries? Hughes: The Deepwater Tano Petroleum Agreement was signed in March 2006. Expiry of the TEN development and production area is in 2Q 2036, although we will have to relinquish some of the area around the Tweneboa gas find two years after production. At the moment, we do not have the opportunity to drill appraisal wells on this area, but we will need to look at this with the government. We will also look again at the surrounding area and satellites and will take into account ITLOS’ decision. Source: Offshore and Tullow

October 2016 USDA report released last week shows that in 2014, the biobased products industry contributed $393 billion and 4.2 million jobs to America's recovering economy. The report also indicates that the sector grew from 2013 to 2014, creating or supporting an additional 220,000 jobs and $24 billion over that period. As one of the four pillars USDA has identified to boost our country's rural economy, USDA has invested heavily in growing the biobased economy.

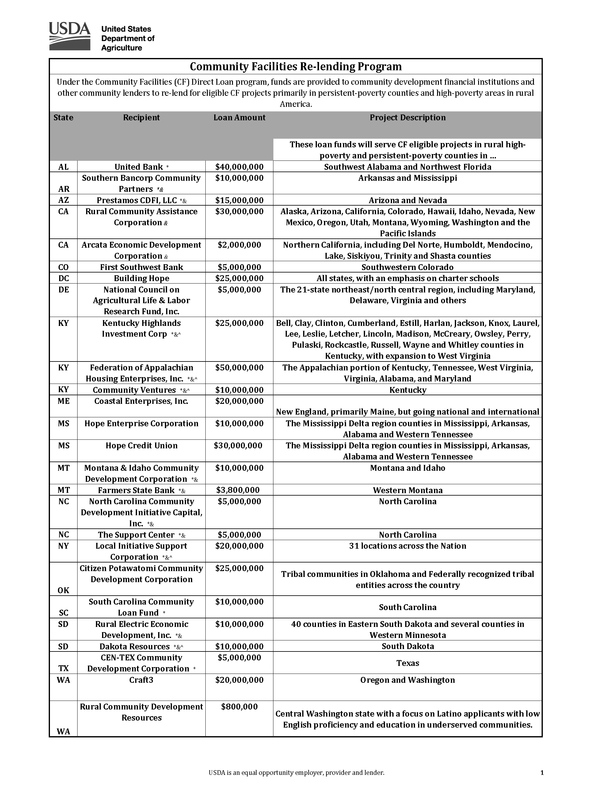

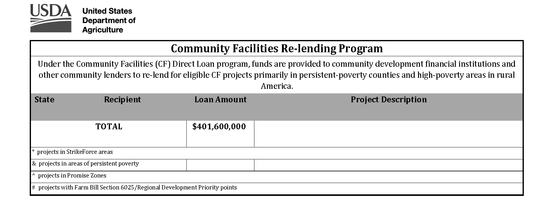

At the same time, we’re working on regional solutions to alleviate long-term poverty, which disproportionately affects rural areas. In an effort to address this, last week USDA unveiled an innovative partnership with community development organizations from across the country, providing $401 million in funds to recipients with a track record of successful programs that help reduce poverty in some of the nation’s most isolated rural communities. Twenty-six community development organizations have been approved to draw upon the funding to help local entities build, acquire, maintain or renovate essential community facilities. The funds also can be used for capacity building and to finance essential community services, such as education, health care and infrastructure. Many of the projects will be in some of the nation's poorest rural areas, such as communities in Appalachia, the colonias along the U.S./Mexico border and in the Mississippi Delta region. Below is a list of the projects.

Source: USDA

Full report in pdf format (142 pages) can be provided upon receive of your request. Our Concierge Services

Independent Global Sales Agents Hiring Announcement

|

| Chick-fil-A is dominating fast food. The company generates more revenue per restaurant than any other fast-food chain in the US, according to QSR magazine. Chick-fil-A's average sales per restaurant in 2015 were $3.9 million. Its fried-chicken competitor KFC sold about $1 million per restaurant that year. |

The sub chain Jason's Deli ranked a distant second with $2.7 million in per-restaurant sales, followed by Whataburger and McDonald's, each with $2.5 million in per-restaurant sales.

So what is the secret to Chick-fil-A's success?

According to a new study from QSR and research firm SeeLevelHX, Chick-fil-A has the best drive-thru service of any of its competitors.

The chain scored the highest marks on employee politeness at the drive thru, according to the study, which compiled data from 2,000 visits to 15 fast-food chains.

Employees said "thank you," smiled, and had a pleasant demeanor during nine out of 10 visits.

The chain also had the second-highest rate of accuracy at the drive thru. Chick-fil-A got orders right 95% of the time, which made it second only to Carl's Jr.'s accuracy rate of 97%.

The only place where Chick-fil-A didn't rank highly was in speed of service.

The average wait time at Chick-fil-A's drive thru is 4 minutes and 16 seconds, which is about 31 seconds longer than the average drive-thru wait time.

The drive thru is an essential element to the fast-food business. It's estimated that 60% to 70% of fast-food chains' business comes through the outside car lanes.

One reason for Chick-fil-A's high scores on service is its face-to-face ordering process, in which employees stand outside and take drive-thru customers' orders using tablet computers.

That leaves less room for error and provides a more personable experience at the drive thru. It's also meant to speed up the ordering process.

The strategy was started by local Chick-fil-A operators in Houston and it's now being rolled out nationwide, according to QSR.

Bass Pro Shops Is Buying Cabela's In a $5.5 Billion Deal

| Bass Pro Shops is buying Cabela's in a $5.5 billion deal that brings together two prominent outfitters for the great outdoors. Bass Pro Shops sells fishing supplies, and Cabela's is a hunting store known for its taxidermy displays. There's plenty of crossover -- especially because both companies sell guns and ammunition. |  |

Cabela said its stockholders would be paid $65.50 in cash per share. Cabela's (CAB) stock jumped 15% at the start of trading.

Johnny Morris, founder of Bass Pro Shops, assured customers in an open letter that "there will be no immediate impact to our stores."

The companies did not immediately respond to CNNMoney messages about whether any of Cabela's 19,000 employees would eventually be laid off or any of its 85 U.S. and Canadian stores closed.

Bass Pro Shops, which is privately held, said it would honor Cabela's rewards cards and credit cards.

Cabela's stores have a distinctive rustic decor featuring displays of stuffed bears, deer, elk and moose. Some of the larger stores resemble theme parks or natural history museums, with extravagant displays of Arctic landscapes with stuffed Musk oxen, or African landscapes with stuffed elephants.

Much of Cabela's merchandise is camouflage and camping gear, including tents and bear-proof food kegs. The company is also known for its so-called gun libraries, green-walled rooms with antique guns for sale, including firearms from both World Wars.

The deal is being financed by Goldman Sachs (GS) and Pamplona.

Sources: Forbes, CNBC, Business Insider and CNN

Johnny Morris, founder of Bass Pro Shops, assured customers in an open letter that "there will be no immediate impact to our stores."

The companies did not immediately respond to CNNMoney messages about whether any of Cabela's 19,000 employees would eventually be laid off or any of its 85 U.S. and Canadian stores closed.

Bass Pro Shops, which is privately held, said it would honor Cabela's rewards cards and credit cards.

Cabela's stores have a distinctive rustic decor featuring displays of stuffed bears, deer, elk and moose. Some of the larger stores resemble theme parks or natural history museums, with extravagant displays of Arctic landscapes with stuffed Musk oxen, or African landscapes with stuffed elephants.

Much of Cabela's merchandise is camouflage and camping gear, including tents and bear-proof food kegs. The company is also known for its so-called gun libraries, green-walled rooms with antique guns for sale, including firearms from both World Wars.

The deal is being financed by Goldman Sachs (GS) and Pamplona.

Sources: Forbes, CNBC, Business Insider and CNN

[Discover more of net lease investment...]

Should you have further questions, please sign-in with our 30-minutes confidential consultation.

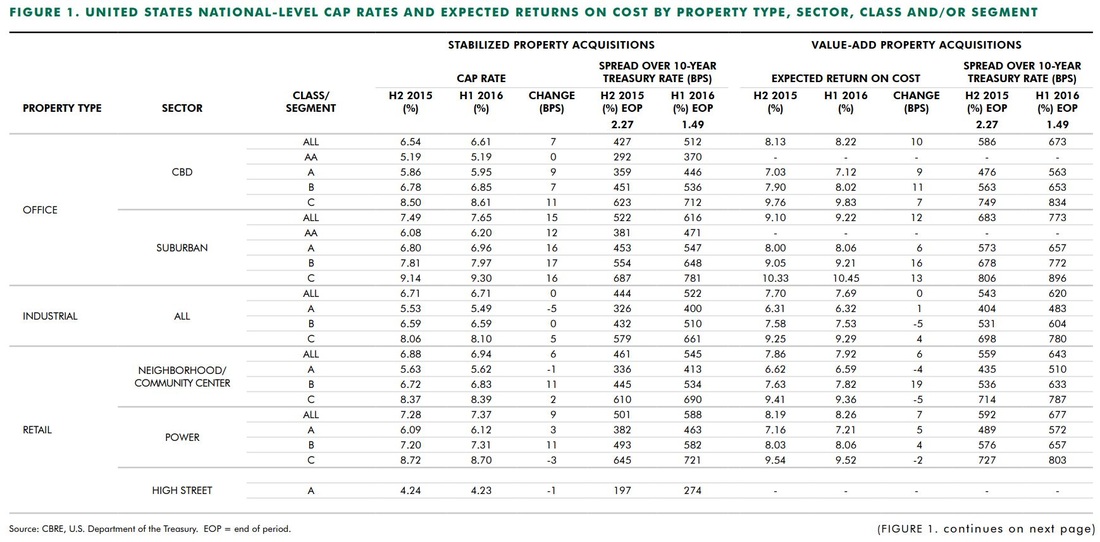

Highlights

• Central Business District (“CBD” or “Downtown”) Office Sector

• Suburban office Sector

• Industrial Sector

• Retail Sector

• Multifamily properties Sector

• Hotel Sector

For all property types, little to no change is anticipated over the next six months in more than 60% of the markets. In markets where change is anticipated, cap rates are more likely to increase rather than decrease.

Central Business District (“CBD” or “Downtown”) Office

Cap rates edged upward for all CBD office classes and tiers in H1 2016 with the exception of Tier II and III Class AA properties. Overall, the increases for both stabilized and value-add acquisitions were generally modest at 7 and 10 bps, respectively.

Suburban office

Suburban office cap rates for stabilized assets and expected returns on cost for value-add acquisitions increased across all classes and, in most cases by a greater amount than those for CBD properties. Stabilized cap rates rose 15 bps, while value-add expected returns on cost increased 12 bps.

Industrial Sector

Industrial cap rates were essentially flat for acquisitions of stabilized assets in H1 2016. The overall rate was 6.71%. Cap rates for stabilized Class A industrial space dropped 5 bps to 5.49%; Class B remained flat at 6.59%; and Class C increased 7 bps to 8.10%. The expected return on cost for value-add assets was stable at 7.69%.

Retail Sector

Cap rates in the retail sector were relatively stable in H1 2016. A slow-down in cap rate compression among prime assets suggests that they may have reached a cyclical low in 2015. Meanwhile, modest cap rate expansion for Class B properties in both the neighborhood/community and power center segments signals investor concern about the future of non-prime assets in increasingly competitive retail markets.

Multifamily properties

Multifamily properties have the lowest overall cap rates of any major sector at 5.26% for stabilized infill and 5.67% for stabilized suburban assets.

The H1 2016 survey revealed virtually unchanged cap rate conditions for stabilized infill and suburban multifamily acquisitions. The only notable movement of cap rates for stabilized assets was slightly downward in both infill and suburban Tier III rates, and in Class C suburban cap rates. Investors are still moving out the risk curve in terms of location and product, and still find value add assets very attractive.

The H1 2016 survey revealed virtually unchanged cap rate conditions for stabilized infill and suburban multifamily acquisitions. The only notable movement of cap rates for stabilized assets was slightly downward in both infill and suburban Tier III rates, and in Class C suburban cap rates. Investors are still moving out the risk curve in terms of location and product, and still find value add assets very attractive.

Hotel Sector

The upward shift of hotel cap rates that began in H1 2015 continued in the first half of 2016, with rates rising across most categories. Movements in hotel cap rates among most CBD and suburban property types showed minimal changes. Low barrier-to-entry hotel categories, such as economy and select-service, experienced slightly larger increases.

Hotels recorded the highest increases in cap rates of any property sector. Cap rates for CBD hotels rose modestly from 5 to 15 bps, while those for suburban hotels rose 8 to 22 bps.

Hotels recorded the highest increases in cap rates of any property sector. Cap rates for CBD hotels rose modestly from 5 to 15 bps, while those for suburban hotels rose 8 to 22 bps.

For all property types, little to no change is anticipated over the next six months in more than 60% of the markets. In markets where change is anticipated, cap rates are more likely to increase rather than decrease. Approximately 20% of markets may experience increases of up to 25 bps, versus only 10% of markets that may experience decreases. Less than 5% of markets are likely to experience movement greater than 25 bps in either direction.

Source: CBRE H1 Report

Source: CBRE H1 Report

[Discover more...]

30-minutes Free Confidential Consultation

If you need further clarifications or interest with net lease commercial real estate investment, please sign-up for our 30-minute Free Confidential Consultation.

- Why the U.S. is a major roadblock for oil output freeze

- Libya Resuming Oil Exports From Some Major Ports

- Record Oil Demand Buffers One Corner of Shipping

- Annual Energy Outlook 2016 Report with Projection to 2040

Why the U.S. Is a Major Roadblock For Oil Output Freeze

The U.S., especially now that it can export crude, is a global threat to market share, it’s not just a threat indirectly through product exports any more

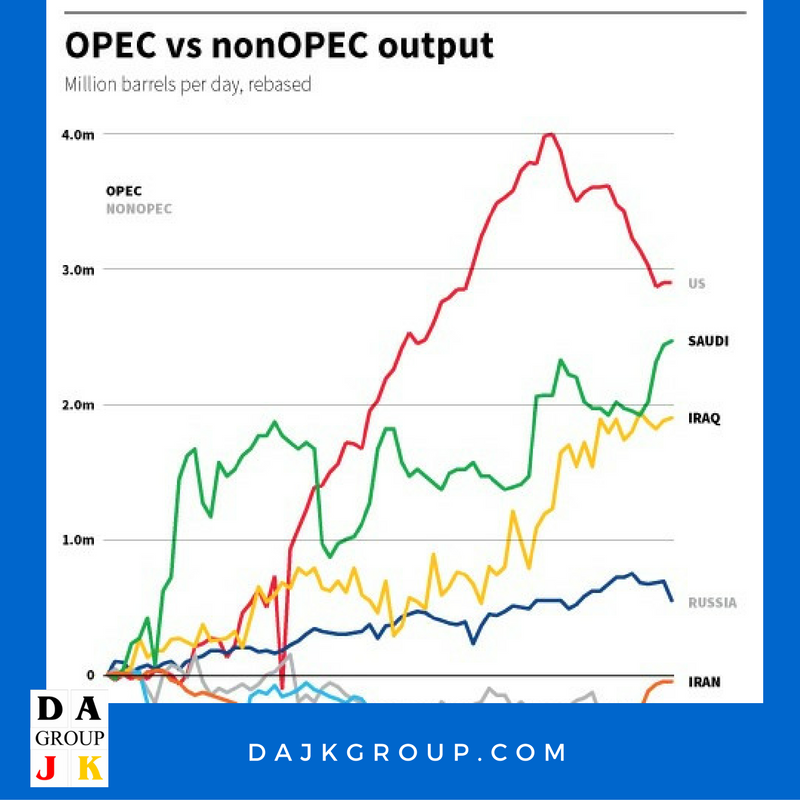

The price of oil has been caught in one of its most volatile couple of weeks in months after OPEC and rival Russia hinted they may discuss a possible output freeze, as demand slows and a global surplus becomes more entrenched. The Organization of the Petroleum Exporting Countries and Russia meet on the sidelines of the International Energy Forum in Algiers in two weeks’ time. The pressure is mounting on both sides to not only freeze output, but possibly even cut it. Whatever the rival factions decide, one producer has managed to top them all in terms of production growth over the last five years and will never be likely to join in any group efforts to control supply. And that is the United States.

Since 2010, thanks to the boom in shale oil production, the United States has witnessed more growth in daily output than any other major producer.

U.S. oil output is around 2.87 million barrels per day higher now than it was six years ago, compared with an increase of 2.47 million bpd from Saudi Arabia and a rise of 1.9 million bpd from Iraq.

In fact, the increase in U.S. production is only just above the collective increase for the whole of OPEC, which comes in at around 3.15 million bpd.

"If OPEC were to cut its production in Algiers, or really freeze its production, then prices would rise, and what producer would benefit the most rapidly from those high prices? It would be the U.S.. We would be back soon enough in a situation where the U.S. will move toward its previous boom-rate of growth and therefore start absorbing market share again," Wood Mackenzie analyst Ann-Louise Hittle said.

"It’s another reason why it's difficult for OPEC to agree to a freeze" she said. "The U.S., especially now that it can export crude, is a global threat to market share, it’s not just a threat indirectly through product exports any more."

In November 2014, OPEC ditched its policy of restraining supply to support the price of oil, which has fallen by more than 40 percent since then to around $46 a barrel LCOc1.

Increases in the likes of Saudi Arabia or Iraq have been countered by losses in Libya and Nigeria or Venezuela, while Iran is just about approaching output levels registered prior to the introduction of Western sanctions in response to Tehran's nuclear program that were lifted in January 2016.

Libya Resuming Oil Exports From Some Major Ports

Libya is resuming oil exports from some of its main ports which forces loyal to eastern commander Khalifa Haftar seized in recent days and has lifted related “force majeuere” contractual clauses, the National Oil Corporation said on Thursday. The north African nation is highly dependent on hydrocarbon revenues and needs oil exports to resume to save its economy from collapse. Conflict since Libya’s 2011 uprising has reduced its oil output to a fraction of the 1.6 million barrels per day the OPEC member once produced. “Exports will resume immediately from Zueitina and Ras Lanuf, and will continue at Brega … exports will resume from Es Sider as soon as possible,” NOC Chairman Mustafa Sanalla said.

He said Libya's U.N.-backed government in Tripoli and a parliament based in eastern Libya both backed reopening the ports which have been controlled by forces loyal to Haftar since Sept 11-12.

Haftar has been an outspoken opponent of the Government of National Accord (GNA) in Tripoli, and his seizure of the four ports from a rival force aligned with the GNA had raised fears of fresh conflict over Libya's oil resources.

"NOC is in charge of the ports," Sanalla said on Thursday, a day after visiting Zueitina. "They are secure, and we have been in contact with our foreign commercial partners."

A Reuters reporter at Zueitina saw large numbers of military vehicles and men belonging to a guard force allied to Haftar's Libyan National Army (LNA).

Western powers had condemned Haftar's seizure of the ports and had said they were ready to prevent any exports attempted outside the GNA's authority.

"(This) had the potential to escalate, with potentially devastating consequences for the nation and our petroleum industry," Sanalla said.

"Instead, we have found a shared interest in letting the oil flow, and the wisdom of that decision needs to be recognized."

U.S. Libya envoy Jonathan Winer called reports of the LNA handing over control of the ports to the NOC a "promising development", writing on Twitter that increased oil production could have an "immediate positive impact".

Libya could raise output to 600,000 barrels per day (bpd) within a month and to 950,000 by the end of the year from about 290,000 currently, Sanalla said this week, but he said NOC would need new funds and blockaded pipelines in southwest Libya would need to be reopened.

Declaring "force majeuere" allows an oil supplier to break a contract because of circumstances beyond its control.

He said Libya's U.N.-backed government in Tripoli and a parliament based in eastern Libya both backed reopening the ports which have been controlled by forces loyal to Haftar since Sept 11-12.

Haftar has been an outspoken opponent of the Government of National Accord (GNA) in Tripoli, and his seizure of the four ports from a rival force aligned with the GNA had raised fears of fresh conflict over Libya's oil resources.

"NOC is in charge of the ports," Sanalla said on Thursday, a day after visiting Zueitina. "They are secure, and we have been in contact with our foreign commercial partners."

A Reuters reporter at Zueitina saw large numbers of military vehicles and men belonging to a guard force allied to Haftar's Libyan National Army (LNA).

Western powers had condemned Haftar's seizure of the ports and had said they were ready to prevent any exports attempted outside the GNA's authority.

"(This) had the potential to escalate, with potentially devastating consequences for the nation and our petroleum industry," Sanalla said.

"Instead, we have found a shared interest in letting the oil flow, and the wisdom of that decision needs to be recognized."

U.S. Libya envoy Jonathan Winer called reports of the LNA handing over control of the ports to the NOC a "promising development", writing on Twitter that increased oil production could have an "immediate positive impact".

Libya could raise output to 600,000 barrels per day (bpd) within a month and to 950,000 by the end of the year from about 290,000 currently, Sanalla said this week, but he said NOC would need new funds and blockaded pipelines in southwest Libya would need to be reopened.

Declaring "force majeuere" allows an oil supplier to break a contract because of circumstances beyond its control.

Record Oil Demand Buffers One Corner of Shipping

Indian carriers are benefiting from surging oil imports Most of the South Asian nation’s fleet comprises tankers As the shipping industry grapples with a prolonged slump in demand, carriers in India are grateful for the bright spot of record domestic fuel consumption. The nation of 1.3 billion people is expanding at the fastest pace among major economies and is set to import an unprecedented amount of crude oil to fuel growth. That’s helping the tanker-heavy fleets of Shipping Corp. of India Ltd., Great Eastern Shipping Co. and Mercator Ltd., India’s three largest carriers. “Because our energy consumption is so high — with the population and the sheer size of the country — demand will continue to rise,” B. B. Sinha, a director and former chairman of Shipping Corp. of India, said in an interview in Mumbai. Oil and liquefied natural gas offer good opportunities, he added.

While a trade slump and industry overcapacity pushed some container lines and bulk carriers to collapse or report losses, the three Indian lines posted profits in the last two fiscal years. Mercator’s shares more than doubled in the past 12 months, bucking a global decline in shipping stocks.

While a trade slump and industry overcapacity pushed some container lines and bulk carriers to collapse or report losses, the three Indian lines posted profits in the last two fiscal years. Mercator’s shares more than doubled in the past 12 months, bucking a global decline in shipping stocks.

Container shipping companies carry a wide range of goods such as clothes, furniture and bananas, while bulk carriers ship unpacked cargo including coal, cement and grains.

“Idling isn’t a threat to us,” said Atul J. Agarwal, executive vice chairman of Mercator, pointing to a rule that gives domestic carriers first right of refusal in tenders for certain shipments.

Shipping rates tumbled after the 2008 global financial crisis and remain depressed. South Korean container line Hanjin Shipping Co., Japan’s Daiichi Chuo KK and dry-bulk shippers Global Maritime Investments Holdings Cyprus Ltd. and Bulk Invest ASA are among companies to have filed for bankruptcy in the past year or so.

Imports account for roughly 80 percent of India’s crude oil needs. The $2 trillion economy is expected to surpass Japan as the world’s third-largest oil user this year, and will be the fastest-growing crude consumer in the world through 2040, International Energy Agency estimates show.

Annual Energy Outlook 2016 Report with Projection to 2040

Projections in the Annual Energy Outlook 2016 (AEO2016) focus on the factors expected to shape U.S. energy markets through 2040. The projections provide a basis for examination and discussion of energy market trends and serve as a starting point for analysis of potential changes in U.S. energy policies, rules, and regulations, as well as the potential role of advanced technologies.

Key updates made for the AEO2016 Reference case include the following:

The Annual Energy Outlook 2016 (AEO2016) Reference case included as part of this complete report (released in July 2016) has been updated from the Annual Energy Outlook 2015 Reference case (released in April 2015). The updated Reference case reflects new legislation and regulations enacted since April 2015, model changes, and data updates. The key model and data updates include:

Macroeconomic

- Updated historical data on industries and employment

- Updated information on natural gas extraction from the National Energy Modeling System (NEMS)

- Extended dynamic Input-Output framework from 2013 to 2040

- Disaggregation of three pulp and paper subindustries included in the NEMS macroeconomic model: pulp and paper mills, paperboard and containers, and all other pulp and paper

- Disaggregated ethanol, flat glass, and lime and gypsum subindustries in the Industrial Output and Employment Model

- Incremental electricity investment required to meet the standards in the U.S. Environmental Protection Agency (EPA) Clean Power Plan (CPP) [7]

- Re-estimated commercial floorspace model, using data from Dodge Data and Analytics, and transformation of floorspace estimates to projected growth rates rather than levels

Full e-Report (256 pages) will be email to you once we receive your request.

Sources: Reuters, Bloomberg, EIA

Libyan Crude Oil Buyer Wanted

Learn more details at Oil Trade page

Author

DAJK GROUP is the place where investors, business owners and entrepreneurs can research and find useful information, insight, resources, advice, guidance and inspiration for acquiring funds for their project, acquisition for their net lease commercial real estate, increasing their assets and running their profitable business.

Archives

July 2023

June 2023

May 2023

August 2019

March 2019

December 2018

October 2018

September 2018

August 2018

July 2018

June 2018

May 2018

April 2018

March 2018

January 2018

December 2017

November 2017

October 2017

September 2017

July 2017

June 2017

May 2017

April 2017

March 2017

January 2017

December 2016

November 2016

October 2016

September 2016

August 2016

July 2016

June 2016

May 2016

April 2016

February 2016

January 2016

December 2015

October 2015

September 2015

August 2015

July 2015

June 2015