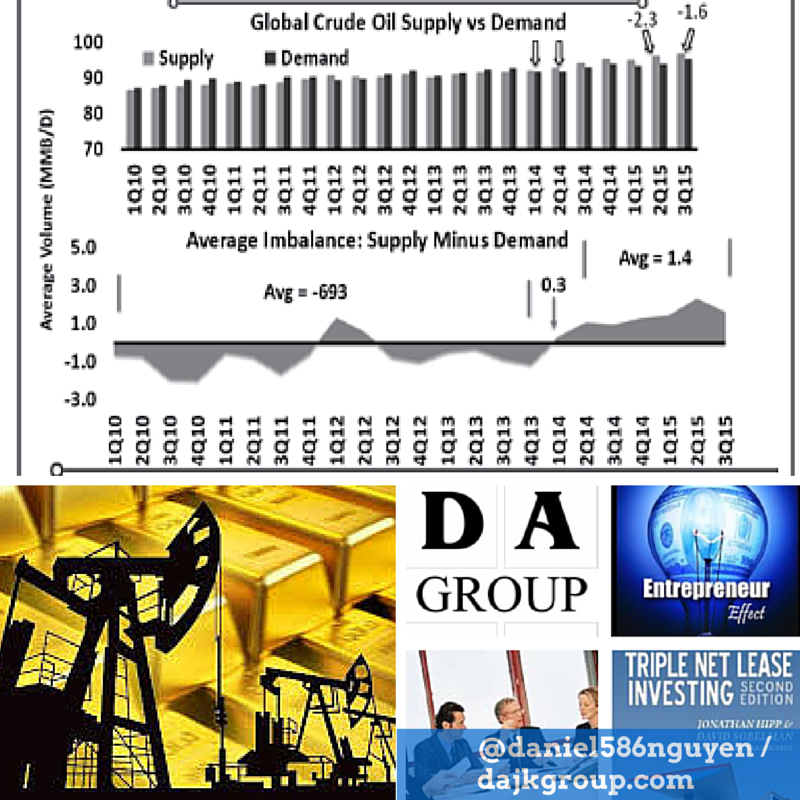

On the other hand, the imminent introduction of Iranian oil onto global markets and the ability of U.S. producers to restart production at the first sign of higher prices is likely to prevent oil from rising much above the $50 to $55 per barrel for the foreseeable future. As 2016 begins to unfold, economists and forecasters are putting together their perspectives on what will drive economic growth for domestic and global (developed and emerging) economies. The consensus seems to be that the most dominant issues will be the prices of oil and other commodities, along with the pace of economic growth in China. Additionally, there is concern about the potential ripple effects that may occur both domestically and around the world in reaction to the decisions of the Federal Reserve as it continues to raise short-term interest rates back to a “normal” level. The price of oil was $37.13 per barrel at the end of 2015. That was a drop of 30.6% for the year, and came on the heels of an even sharper decline (45.5%) in 2014. This has created a massive global transfer of wealth from oil producers to consumers. In the long run, this is a good thing for the United States, because consumption accounts for two-thirds of our economy. The extra disposable income gained from lower energy prices will allow households to increase their spending. However, in the short term, lower oil prices have reduced the incentive to invest in drilling and exploring, which in turn has acted as a drag on domestic GDP. On a global level, reduced revenues are squeezing the budgets of many oil-producing countries, which could lead to even higher levels of political instability.  It is not just oil. Prices of many other commodities, from food to industrial metals, have also fallen to near-record lows. In recent years, many emerging economies (China, Russia, Brazil, Mexico, Chile, etc.) spent heavily to develop the infrastructure needed to deliver their products to customers around the world. Now that the demand for these products has fallen, this has left many emerging nations with enormous debt loads, as much of their infrastructure development was financed by borrowing (frequently in dollars). Rising interest rates and less-favorable currency exchange rates have further increased the financial pressures on these countries, which need to continue producing in order to generate revenue to service their debts, even if they are producing below cost. The result is continued supply in an already weak market that is keeping prices low. This also applies to oil, but the dynamic is different this time. In the past, when prices fell, supply was curtailed in response, thereby bringing the supply/demand equation back into equilibrium As for the U.S., we anticipate the pace of economic growth to increase somewhat in 2016 (reaching the range of 2.2% to 2.7%) due in large part to increased consumer spending. We expect inflationary pressures to move up ever so slightly, held down in part by low commodity prices, which account for about one-third of most inflation measurements. We also believe the Fed will raise short-term interest rates (50 or 75 basis points in 2016), which is below its forecast of 100 bps. Outlook for Oil: Ready for a Rebound?Producers, consumers, and investors have witnessed a stunning 70% drop in the price of oil over the last 18 months. This has resulted in huge declines in employment in the energy and mining industries, and lower gasoline prices for consumers. It has also led to a significant increase in economic pressure among those countries heavily dependent on oil revenues for government spending. In every free market, price is dictated by supply and demand. In 2015, demand growth was strong, but not as strong as one would expect given the freefall in prices. Over half of the annual growth in demand for oil in the latter part of the last decade came from China. As a result, China’s much-publicized economic slowdown clearly has had a negative impact on overall demand. The rise of shale oil production over the past decade in the United States has greatly diminished OPEC’s ability to set prices in the marketplace. Despite falling prices, OPEC has maintained production levels in order to force higher-cost producers out of the market. So far, this strategy has largely failed, as production has remained relatively stable. Congress recently passed a $1.1 trillion spending measure that provides tax credits for the use of alternative energy sources (e.g., solar, wind) and lifts the 40-year-old oil export ban. Congress recently passed a $1.1 trillion spending measure that provides tax credits for the use of alternative energy sources (e.g., solar, wind) and lifts the 40-year-old oil export ban. In the long run, increased use of renewable energy sources could crimp demand for fossil fuels, but in the near term, it should result in an increase in domestic oil production. North America’s growing production capacity has diminished OPEC’s price-setting ability on global oil markets, and this trend is likely to continue as domestic production increases.

The decline in oil prices has resulted in massive global rig reductions, most notably in the U.S. and Canada. International rig count is down only 16%, primarily because of larger/longer projects and because national governments need oil revenues to balance their budgets. Despite the sharp reduction in rig count, U.S. crude oil production is still high. Producers have become increasingly efficient by using newer drilling techniques and focusing on core acreage areas. They are pumping more from fewer rigs. With large debt burdens that require servicing, oil exploration companies have chosen to keep the taps flowing in order to generate revenue. Shutting down rigs and cutting jobs has allowed them to lower their breakeven prices, but most U.S. shale oil producers are losing money at the current price of oil ($31.41 per barrel as of January 11, 2016). The excess supply is rapidly filling the capacity of storage facilities. This is an unsustainable situation, and production is beginning to decline as smaller producers exit the business. We believe that overall weak global demand and limited excess capacity will constrain production in the near term, helping to keep a floor under prices. On the other hand, the imminent introduction of Iranian oil onto global markets and the ability of U.S. producers to restart production at the first sign of higher prices is likely to prevent oil from rising much above the $50 to $55 per barrel for the foreseeable future.

0 Comments

Leave a Reply. |

AuthorDAJK GROUP is the place where investors, business owners and entrepreneurs can research and find useful information, insight, resources, advice, guidance and inspiration for acquiring funds for their project, acquisition for their net lease commercial real estate, increasing their assets and running their profitable business. Archives

July 2023

Categories |

Services |

Company |

|